Skip to content

Skip to content Have you ever heard of a life insurance policy or retirement account that pays out directly to your family, completely skipping the lengthy and often stressful court process? That’s the magic of a non-probate asset. These assets transfer automatically to a designated person upon death, bypassing the formal court supervision known as probate. We understand that navigating these topics can be emotionally challenging, and our goal is to provide clear, compassionate guidance to help your family feel secure.

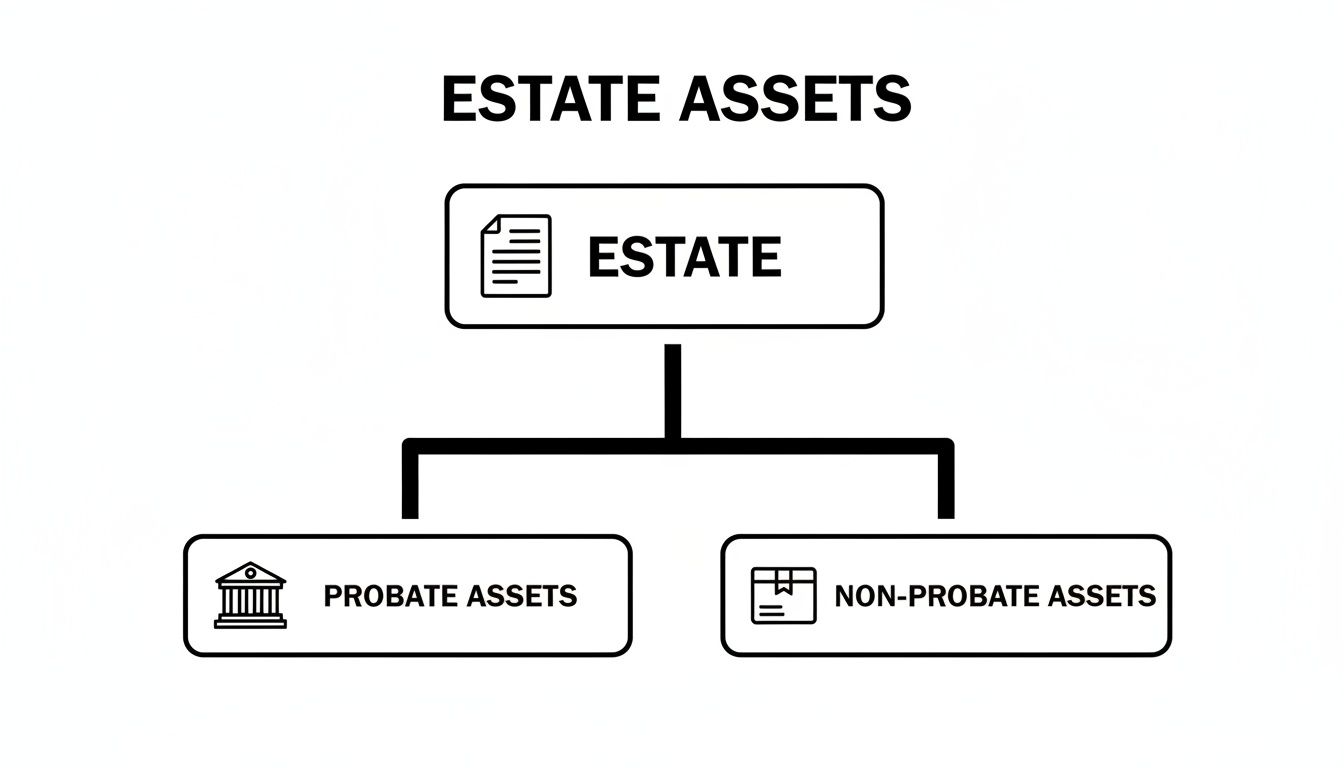

Understanding the Role of Non-Probate Assets in Texas

When a loved one passes away in Texas, their property is generally split into two buckets: probate assets and non-probate assets.

Think of it this way: probate assets are like standard mail that has to be opened, sorted, and officially approved by a Texas probate court before it can be delivered. On the other hand, non-probate assets are like express packages, pre-addressed directly to your loved ones. They arrive much faster because they follow a completely different set of rules.

This distinction isn't just a minor legal detail; it's the foundation of a solid estate plan. For Texas families, figuring out how these assets work can provide critical financial stability and peace of mind during an already difficult time.

How These Assets Bypass the Court System

The key difference comes down to how ownership is transferred. Non-probate assets are controlled by legal contracts or how they are titled, not by the instructions written in a will.

A key concept in the Texas Estates Code is that many assets can pass to beneficiaries without needing a judge's permission. This happens because the transfer is governed by a contract—like the beneficiary designation form you filled out when you opened an account or bought a policy. That contract legally overrides what your will says about that specific asset.

This contractual transfer is an incredibly powerful tool. It means the funds from a 401(k) or the proceeds from a life insurance policy can get into your family's hands much more quickly than assets that have to slog through the entire probate process, which can take months or even years in complicated situations.

Why This Matters for Your Family’s Security

Getting your non-probate assets set up correctly ensures your financial wishes are carried out exactly as you intend, without unnecessary delays or court interference. Some of the most common examples that work this way include:

- Life Insurance Policies: The death benefit is paid directly to the person you named on the beneficiary form.

- Retirement Accounts (IRAs, 401(k)s): Funds are transferred straight to the designated beneficiaries, keeping them out of the probate estate.

- Payable-on-Death (POD) Bank Accounts: The money in the account becomes immediately payable to the named beneficiary.

- Jointly Owned Property with Right of Survivorship: Ownership automatically passes to the surviving joint owner.

Simply failing to understand how this works can lead to unintended consequences, creating confusion and potential disputes among heirs. By learning the basics of Estate Planning, you can ensure your legacy is protected. For personalized guidance on how these assets fit into your family's unique situation, we invite you to Schedule a free consultation with our experienced team.

The Major Types of Non Probate Assets

Think of your estate plan as a roadmap for your assets. Some assets take the local roads, winding through the probate court system. Non-probate assets, on the other hand, are like taking the expressway—they have a direct, pre-planned route to their destination, bypassing all the traffic.

How an asset is legally structured determines which path it takes after you're gone.

As you can see, what’s written in your will doesn't control everything. The legal title and beneficiary forms often have the final say. Let's break down the most common types of these "expressway" assets you'll find here in Texas.

Assets with Beneficiary Designations

The most straightforward way to create a non-probate asset is with a beneficiary designation. This is simply a form you fill out with a financial institution, creating a legally binding contract.

This document tells the institution exactly who gets the asset when you pass away, and it completely overrides what your will might say. It’s a powerful tool for ensuring a direct and quick transfer of wealth.

Common examples include:

- Life Insurance Policies: The death benefit is paid directly to the people you’ve named on the policy.

- Retirement Accounts: This covers your 401(k)s, IRAs, 403(b)s, and pensions.

- Annuities: Any remaining funds go straight to your chosen beneficiary.

Here's a hypothetical scenario: Maria named her son, David, as the sole beneficiary on her $250,000 life insurance policy. Even if her will states her entire estate should be split equally with her daughter, that $250,000 goes directly to David. The beneficiary form is a separate, binding contract that the will cannot change.

Accounts with Payable on Death or Transfer on Death Instructions

Another simple way to keep assets out of probate is by using Payable-on-Death (POD) and Transfer-on-Death (TOD) designations. These are easy instructions you can add to your bank and investment accounts.

A POD instruction is for bank accounts—think checking, savings, and CDs. A TOD instruction is used for securities like stocks, bonds, and brokerage accounts. When you pass away, your named beneficiary just has to show a death certificate to the bank or brokerage firm to claim the funds. It’s that simple.

These tools are becoming more important than ever. Shockingly, only 32% of Americans have a will as of 2024, a significant drop from past years. This trend underscores just how critical non-probate tools are for ensuring your assets go where you want them to, with or without a formal will.

Assets Held in a Revocable Living Trust

A Revocable Living Trust is a more comprehensive tool for avoiding probate. Think of it as creating a private company to hold and manage your property. You create the trust, transfer your assets into it, and manage them yourself as the trustee while you're alive.

Because the trust owns the assets—not you personally—there’s nothing for the probate court to oversee when you die. The person you’ve named as your successor trustee simply steps in and follows the rules you laid out in the trust to distribute the assets to your beneficiaries.

This approach offers significant privacy and control, keeping your family’s business out of the public record at the Dallas County or Travis County courthouse. For a deeper dive into how these tools compare, it's worth understanding the differences between a living trust and a will.

Property Owned with Right of Survivorship

Finally, the way a property is titled can automatically make it a non-probate asset. When two or more people own property as "joint tenants with right of survivorship," the surviving owner automatically gets the whole thing.

This is a very common setup for:

- Real Estate: Most married couples in Texas own their home this way.

- Bank Accounts: It’s standard for couples to have joint checking or savings accounts.

- Vehicles: A car title can easily be held jointly with this designation.

When one owner passes away, their share just disappears, and the surviving owner (or owners) now owns 100% of the property. No court, no probate, no fuss. This is a fundamental concept in the Texas Estates Code that provides immediate access and continuity for the survivor.

To help you keep it all straight, here’s a quick-glance table comparing common probate and non-probate assets in Texas.

Common Non-Probate vs Probate Assets in Texas

| Asset Type | Typically a Non-Probate Asset (Bypasses the Will) | Typically a Probate Asset (Controlled by the Will) |

|---|---|---|

| Bank Accounts | Joint accounts with right of survivorship; accounts with a Payable-on-Death (POD) beneficiary. | Accounts owned solely by the decedent with no POD beneficiary. |

| Real Estate | Property owned as "joint tenants with right of survivorship"; property with a Transfer-on-Death Deed (TODD). | Property owned solely by the decedent or as "tenants in common." |

| Retirement Accounts | IRAs, 401(k)s, 403(b)s with a named beneficiary (other than the estate). | Accounts where the estate is the named beneficiary or no beneficiary is named. |

| Life Insurance | Policies with a named beneficiary (other than the estate). | Policies where the estate is the named beneficiary or no beneficiary is listed. |

| Investment Accounts | Brokerage accounts with a Transfer-on-Death (TOD) beneficiary. | Brokerage accounts owned solely by the decedent with no TOD beneficiary. |

| Vehicles | Titled jointly with right of survivorship. | Titled solely in the decedent's name. |

| Trust Assets | Assets properly transferred into a living trust during the decedent's lifetime. | Assets never transferred into the trust; assets distributed via a testamentary trust (created in a will). |

| Personal Property | Typically does not have a non-probate mechanism. | Furniture, jewelry, art, collectibles, and other personal belongings. |

This table should give you a solid starting point for identifying which of your loved one's assets will need to go through the court process and which can be handled directly.

How Guardianship Proceedings Affect Non Probate Assets

When a loved one can no longer make their own decisions, stepping in to establish a guardianship can feel like a necessary and compassionate move. This legal process, handled by courts like the Harris County Probate Court, appoints a guardian to manage the affairs of an incapacitated person, known as the "ward." But here's where things get tricky: many families are caught off guard by the strict limits a guardian faces when dealing with non probate assets.

A huge and critical misunderstanding is that a guardian can simply change beneficiaries on accounts like life insurance policies, IRAs, or payable-on-death (POD) bank accounts. That's just not the case in Texas. Those beneficiary designations are treated as legally binding contracts that spell out the original wishes of the account holder.

The Texas Estates Code, specifically Title 3, Subtitle G, is very clear on this. A guardian's job is to manage the ward's property for their day-to-day care and well-being—not to rewrite their estate plan. This is a crucial safeguard, preventing a guardian from redirecting a ward’s legacy and ensuring the assets go to the people the ward chose when they were of sound mind.

The Guardian’s Limited Powers

While a guardian holds significant responsibility, their power over non probate assets is deliberately restricted. If a guardian needs to make any changes that would affect the ward’s estate plan, they almost always have to get a specific court order first.

For instance, a guardian can't just decide on their own to:

- Change a life insurance beneficiary from the ward's brother to themselves, even if they are providing all the care.

- Swap out the beneficiary on a 401(k) to someone who wasn't originally named.

- Cash out an annuity that already has a designated beneficiary, unless they can prove to a judge that the funds are absolutely essential for the ward's immediate care.

These rules aren't just red tape; they are vital protections. They shield the incapacitated person from potential exploitation and make sure that the estate planning decisions they made years ago are honored.

A core principle of Texas guardianship law is to act in the best interest of the incapacitated person while interfering with their personal liberties and property rights as little as possible. Preserving their chosen beneficiaries on non probate assets is a perfect example of this principle in action.

A Common Scenario Guardians Face

Picture this: Sarah is the court-appointed guardian for her father, Michael, who has advanced dementia. The nursing home bills are piling up, and Sarah needs to find the money to pay for his care. She discovers he has a sizable 401(k), but the beneficiary isn't her—it's her uncle.

Sarah can't just call the 401(k) company and redirect the funds to pay the bills. She would have to go back to court, file a formal request, and provide detailed financial proof that there's no other way to pay for Michael's care. Even with all that, a judge might be hesitant to touch a designated beneficiary, especially if there are other assets that could be used first.

This scenario highlights a major challenge for families. The very assets designed to be easy to access after death (non probate assets) can become the most difficult for a guardian to manage during the person's lifetime.

Proactive Planning Is the Best Solution

The absolute best way to sidestep these painful situations is to plan before an illness or accident happens. A well-drafted Durable Power of Attorney can give a trusted agent specific authority to manage financial accounts, often providing far more flexibility than a guardianship allows. This is a key alternative to guardianship that every family should consider.

Understanding how these different legal tools work together is key. For a deeper dive into this specific topic, our guide on how guardianship impacts life insurance policies in Texas provides more detailed insights.

If you are thinking about guardianship or are already a guardian struggling with non probate assets, you don't have to navigate this alone. Schedule a free consultation with The Law Office of Bryan Fagan, and let our team provide the clarity and guidance your family needs.

Common Mistakes to Avoid with Non-Probate Assets

Even the most buttoned-up estate plans can come apart at the seams because of a few small oversights. When it comes to non-probate assets, simple mistakes can spiral into major headaches, bitter family disputes, and outcomes you absolutely never intended. Knowing the common pitfalls is the first step toward making sure your assets go exactly where you want them to go.

These assets operate on contracts, not just good intentions. By learning from where others have gone wrong, you can ensure your estate plan works smoothly and protects the people you love.

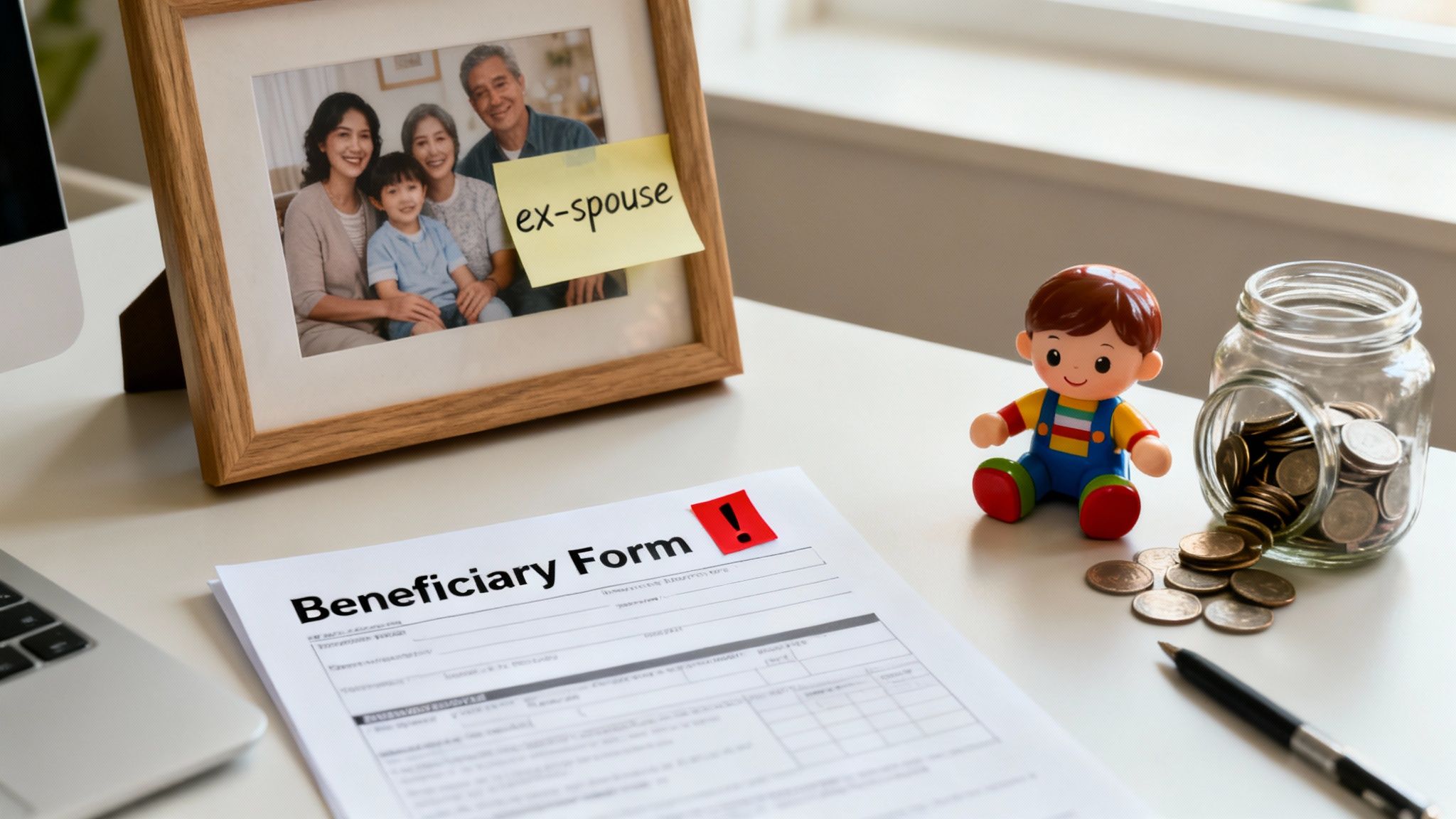

Outdated Beneficiary Designations

Life changes. Beneficiary forms often don't. This is, without a doubt, the most common and devastating mistake we see families run into. A designation you made years ago remains legally binding, no matter what has happened since—divorce, remarriage, you name it.

Picture this: John named his wife as the beneficiary on his sizable 401(k) back in 2010. They divorced in 2018, and John remarried in 2020 but never got around to updating his 401(k) paperwork. When he passes away, that entire retirement account—often a person’s largest single asset—will legally go to his ex-wife, not his current spouse or children. It happens more than you think.

In Texas, a divorce decree automatically voids a beneficiary designation naming an ex-spouse for certain assets, as laid out in the Texas Estates Code. But don't rely on this. Federally regulated plans like 401(k)s often follow their own rules, which can still result in an ex-spouse inheriting if the form isn't updated. Proactive updates are the only safe bet.

Regularly reviewing these forms after any major life event isn't just a good idea—it's a critical part of keeping your estate plan alive and well.

Forgetting Contingent Beneficiaries

Every beneficiary form gives you the option to name both a primary and a contingent (or secondary) beneficiary. Think of it as your Plan A and Plan B. The primary beneficiary is your first choice. The contingent beneficiary is the backup who inherits only if your first choice has already passed away.

Forgetting to name a contingent beneficiary can create a huge mess. If your primary beneficiary dies before you do, that asset may be forced right back into your probate estate. This completely defeats the purpose of setting it up as a non-probate asset, throwing it into the court system where it will face delays and potential creditor claims.

Naming a Minor Directly

It seems like the most natural thing in the world to name your child or grandchild as a beneficiary. But naming a minor directly on a life insurance policy or retirement account can trigger a legal and financial nightmare. Financial institutions simply cannot hand over large sums of money to a minor.

When this happens, your family is forced to go to court—often a probate court in Tarrant County or Bexar County—to get a legal guardian of the estate appointed to manage the funds. This process is:

- Costly: It means court fees and paying for an attorney.

- Time-Consuming: The process can drag on for months, leaving the money tied up when your family might need it most.

- Restrictive: The court will supervise how every dollar is spent until the child turns 18.

A much better strategy is to set up a trust for the minor's benefit, like a testamentary trust in your will, or open a Uniform Transfers to Minors Act (UTMA) account. You then name that trust or the UTMA custodian as the beneficiary, ensuring the funds are managed responsibly without unnecessary court intervention.

Mistakes with non-probate assets can easily derail your best intentions. If you’re worried that your current designations no longer reflect your wishes, it's time to take action. Schedule a free consultation with The Law Office of Bryan Fagan to review your plan and gain the peace of mind that your family will be cared for properly.

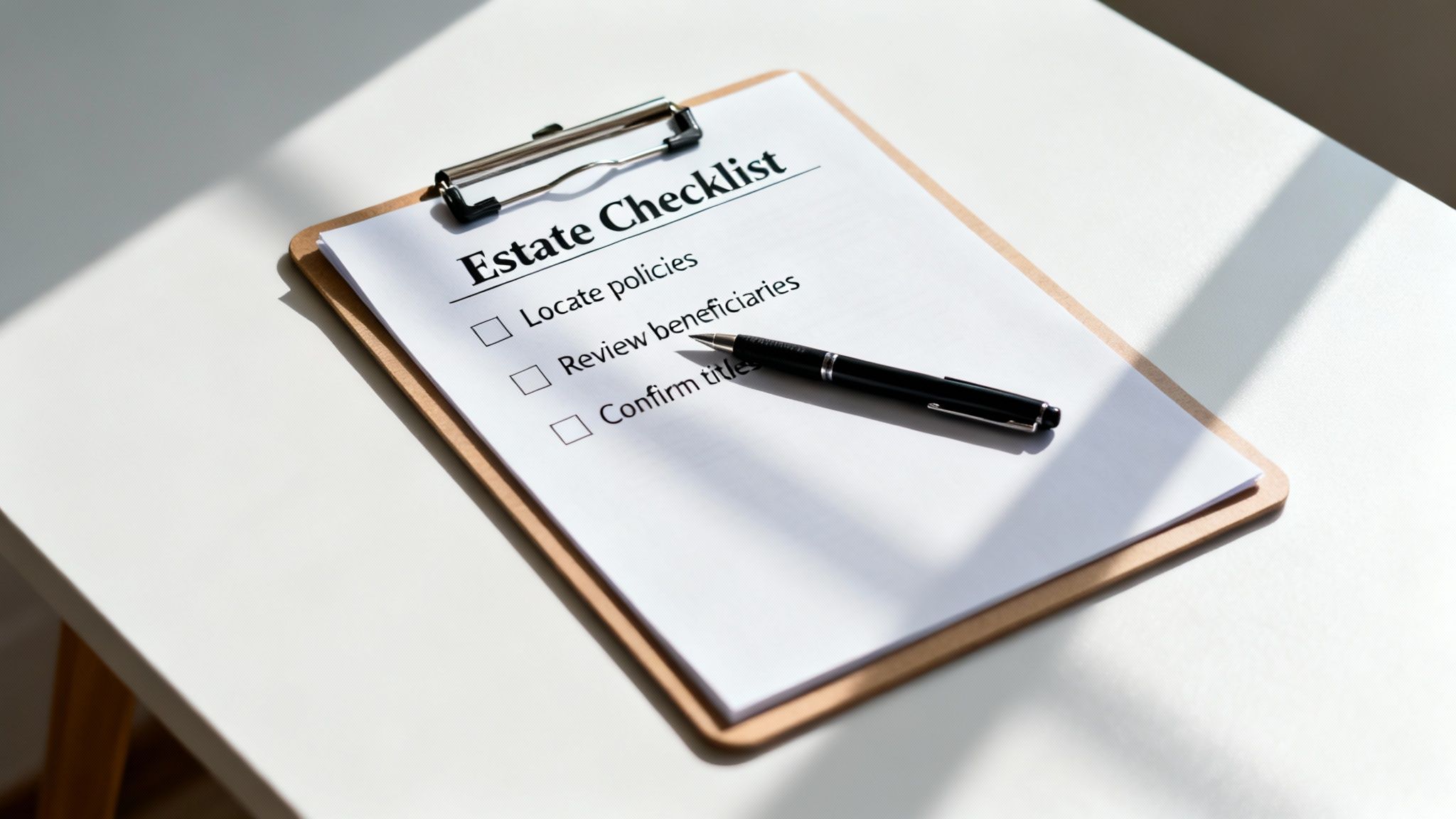

Your Checklist for Managing Non-Probate Assets

It’s one thing to understand the concept of non-probate assets, but it’s another thing entirely to get them organized. This checklist is all about moving from theory to action, giving you clear, practical steps to make sure your assets are lined up exactly with your wishes.

Think of this as a personal audit for your estate. A couple of hours spent now can honestly save your family months of stress and confusion down the road.

Step 1: Locate and Organize Key Documents

First things first, you can't review what you can't find. The initial step is to gather all the important financial paperwork in one place.

- Insurance Policies: Pull out every life insurance and annuity contract.

- Retirement Accounts: Find the most recent statements for any 401(k)s, IRAs, or pensions.

- Bank and Investment Accounts: Collect statements from all your checking, savings, and brokerage accounts.

- Real Estate Deeds: Locate the deeds for any property you own, especially your home.

Getting these documents together gives you a complete financial picture and sets the stage for everything else.

Step 2: Review Every Beneficiary Designation

This is, without a doubt, the most crucial step. A beneficiary designation form is a legal contract that overrides your will. It dictates who gets the asset, period.

You need to contact each financial institution and insurance company and ask for a copy of your current beneficiary forms. Don't just rely on memory—it's too important. When you get the forms, verify:

- Primary Beneficiary: Is the person listed still your first choice? Life changes, and these forms need to keep up.

- Contingent Beneficiary: What if your primary beneficiary can't inherit? You absolutely need a backup named.

- Spelling and Details: A simple typo in a name or a wrong birthdate can cause major administrative headaches for your loved ones.

Step 3: Confirm Legal Titling on Property and Accounts

How an asset is titled can be the very thing that makes it a non-probate asset. You have to check that your joint assets are set up to transfer smoothly.

For any property you own with someone else, look for the magic words: "with right of survivorship." Without this specific phrase, a co-owner's share could get stuck in probate, creating a nightmare for the surviving owner. Check your deeds and bank account agreements to be sure the titling matches your intent.

This simple review ensures that jointly owned real estate or bank accounts will pass directly to the surviving owner, just like you planned.

The modern financial world is massive. Global financial assets hit an incredible EUR 239 trillion by the end of 2023, with securities—many of which can be structured as non-probate assets—making up 42.8% of that total. For Texas families, this explosion in financial instruments makes it more important than ever to manage them correctly. Taking the time for a full review protects your hard-earned portfolio.

Running through this checklist is a fantastic start. But to make sure all of your estate planning documents are working together seamlessly, nothing beats professional guidance. If you find any issues or just have questions, our team is here to help.

When You Need to Speak with a Probate Attorney

While this guide gives you a solid game plan, some situations involving non-probate assets are just too complex and high-stakes to go it alone. Knowing the red flags that signal it's time for professional legal advice is a smart move to protect your family. Reaching out for help isn’t a sign of failure—it’s a sign you’re committed to getting things right.

Think of it like this: you can handle a common cold, but for a serious diagnosis, you see a specialist. The same logic applies to estate planning and administration.

Key Moments to Call for Legal Guidance

Certain scenarios should be an immediate trigger to pick up the phone and call an attorney. These are the situations where one small misstep can spiral into lasting financial damage and bitter family conflict. Don't hesitate if you run into any of these issues:

- Conflicting Documents: You find a will that says one thing, but a beneficiary form says another, leaving everyone confused about who inherits what.

- Family Disputes: A fight breaks out over a joint bank account, or someone claims a beneficiary designation was signed under pressure or duress.

- Guardianship Needs: You need to access a loved one's non-probate funds to pay for their medical care but have no idea how to do it legally.

- Outdated Designations: You discover an ex-spouse is still the named beneficiary on a life insurance policy or a hefty retirement account.

Why Professional Advice Is So Important

A seasoned probate attorney does a lot more than just fill out forms. They bring clarity to tangled situations, serve as a neutral third party during family disagreements, and make sure every action you take is fully compliant with the Texas Estates Code.

This is especially critical for families managing significant wealth. High-net-worth individuals understand the power of strategic planning. In 2023, the global population of individuals with over $1 million in investable assets grew, with their combined wealth hitting a staggering $86.8 trillion. For Texas families with investment accounts, retirement funds, and other major holdings, making sure non-probate assets work in harmony with a will and potential guardianship is absolutely essential. You can learn more about these global wealth trends and what they mean for financial planning.

At The Law Office of Bryan Fagan, we have years of experience navigating the complexities of probate and guardianship in courts from Dallas to San Antonio. We’re here to give you the peace of mind that comes from knowing your family’s future is secure.

If any of these challenges sound familiar, don't wait for a small problem to become a full-blown crisis. Schedule a free consultation with our compassionate legal team today and get the clear, personal guidance your family deserves.

Frequently Asked Questions About Texas Non Probate Assets

When you start digging into the details of estate planning, a lot of specific questions pop up. To help bring some clarity, we’ve put together answers to the most common things Texas families ask about non probate assets and how they really work.

Can a Will Override a Beneficiary Designation in Texas?

This is one of the most critical questions we hear, and the answer is almost always a firm no. A beneficiary designation on an account like a life insurance policy or a 401(k) is a legal contract between you and the company holding the asset. That contract almost always wins out over whatever your will says.

Think of it like this: your will is the playbook for your probate assets, but your beneficiary forms are the playbook for your non-probate assets. They are two separate sets of instructions for two totally different kinds of property. The only real exception is if you name "my estate" as the beneficiary or forget to name one at all. In that case, the asset gets pulled back into the probate process.

Key Takeaway: You can't rely on your will to "fix" an old or incorrect beneficiary form. For that specific account, the form itself is the final word. The only way to be sure your wishes are followed is to regularly check and update these designations yourself.

What Happens if My Beneficiary Dies Before Me?

It’s a scenario that happens more often than you'd think, and it's smart to plan for it. If your primary beneficiary passes away before you do and you haven't named a backup, things can get complicated fast. This is exactly why financial institutions give you the option to name a contingent beneficiary.

- If you have a contingent beneficiary: The asset will pass directly to them, smoothly and outside of probate, just like you wanted.

- If you don't have a contingent beneficiary: The asset will most likely be paid to your probate estate. It immediately becomes a probate asset, which means it’s now subject to the instructions in your will (or Texas intestacy laws if you don't have one), potential claims from creditors, and the usual court delays.

Are Non Probate Assets Protected from Creditors in Texas?

This is another area where the answer is "it depends." While most assets that go through probate are fair game for paying off a decedent's debts, some non probate assets get special protection under Texas law.

For example, retirement funds like 401(k)s and IRAs are generally shielded from the deceased person’s creditors. The same goes for life insurance proceeds paid to a specific person (not the estate). But money in a joint bank account might not have that same strong protection. The rules can be tricky, and it's a huge mistake to assume all non-probate assets are creditor-proof. An experienced attorney can look at your specific assets and tell you what's protected and what's not.

Making sure your will, trusts, and beneficiary designations all work together requires careful planning and a solid understanding of Texas law. If you have questions about your own non probate assets or need help getting your entire estate plan in sync, The Law Office of Bryan Fagan, PLLC is here to offer the clear, compassionate guidance your family deserves. Schedule a free, no-obligation consultation today by visiting our website.