Skip to content

Skip to content You walk into the bank with what you believe are the right papers. Maybe it's a power of attorney for your mother, Letters of Guardianship for your adult son, or probate documents after a death in the family. You're not there to do anything unusual. You're trying to pay for care, keep utilities on, or move money where it needs to go.

Then the banker says they can't honor your authority.

That moment feels personal, but it usually isn't. It's a mix of internal bank policy, legal caution, and frontline employees who don't want to make the wrong call. The core problem is that your family's bills don't pause while the bank “reviews” your paperwork. Caregivers still expect payment. Facilities still draft monthly charges. Prescriptions still need to be filled.

In Texas, what happens when a bank refuses to recognize your authority often turns into two separate problems. First, you need to challenge or fix the refusal itself. Second, you need a short-term plan to keep essential expenses moving without creating more legal trouble for yourself. Families usually focus on the first issue and underestimate the second.

That's where a lot of articles stop too soon. Many explain whether a Texas bank can refuse a power of attorney, but few explain what to do next when groceries, rent, or in-home care can't wait, as noted in guidance on Texas bank refusal and powers of attorney.

A Frustrating Barrier at the Bank

A daughter in Harris County brings a signed power of attorney to her father's bank in Houston. He's had a health decline, and she needs to pay his assisted living bill. The branch employee studies the document, disappears into the back office, and returns with a polite refusal. No access. No payment. No timeline.

A son in Dallas County has Letters of Guardianship and assumes that will settle it. Instead, the bank asks for additional review. Meanwhile, automatic drafts are hitting an account he can't fully manage yet, and he's worried about missing a payment tied to his mother's medical support.

Those stories are common. The legal paper may be valid, but the bank may still slow everything down. For families, the practical stress is immediate. The question isn't just whether the bank is wrong. It's how to keep life functioning while the dispute is pending.

The hardest part for most families isn't the legal principle. It's handling the next few days without making a costly mistake.

Texas families often come to a guardianship lawyer after they've already argued with the branch, made multiple calls, and gotten nowhere. That usually makes the situation feel worse. Bank employees become defensive. Family members become exhausted. Important details get lost.

The better approach is calmer and more methodical.

What this usually affects first

The first disruption is rarely an abstract financial issue. It's something basic:

- Monthly care costs: Assisted living, memory care, sitters, or home health invoices still come due.

- Household bills: Mortgage, rent, taxes, insurance, and utilities don't stop because a bank flagged your paperwork.

- Medical support: Co-pays, equipment, prescriptions, and transportation often need quick payment.

- Family reimbursement problems: A relative starts paying expenses out of pocket and later struggles to document what was proper and what wasn't.

The good news

Most bank-authority disputes are solvable. Some are resolved by presenting cleaner documents and reaching the right department. Others need probate court involvement. If the issue involves guardianship, Texas Estates Code Title 3, Subtitle G is often central because that part of Texas law governs guardianship procedure, duties, court oversight, and the authority created by court appointment.

If your authority comes from a guardianship, the bank's refusal isn't just annoying. It may interfere with a court-supervised fiduciary relationship. That's one reason it's so important to respond in an organized way instead of improvising.

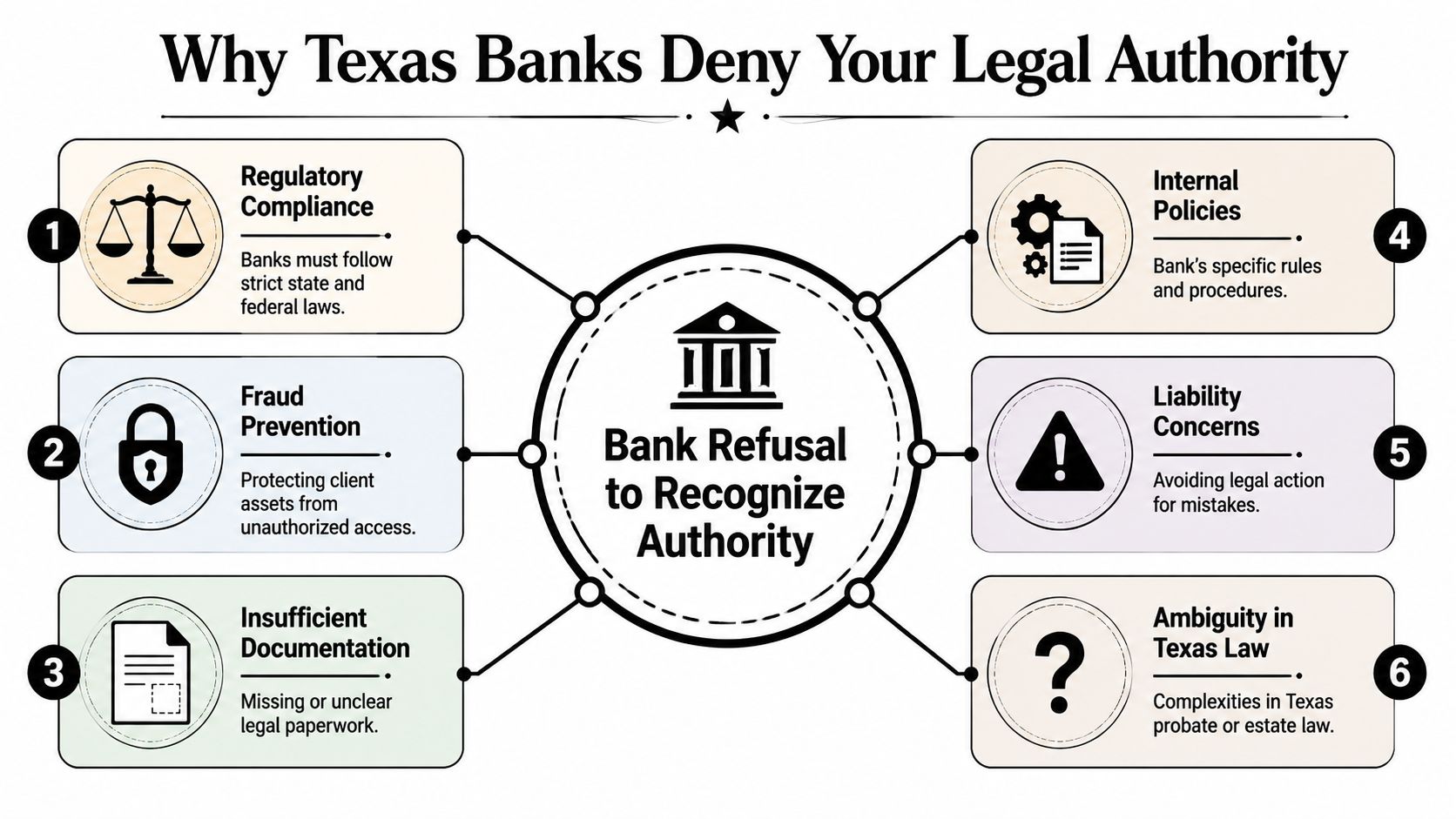

Why Texas Banks Deny Your Legal Authority

Banks don't usually refuse authority because they enjoy making families miserable. They refuse because the wrong decision can expose them to fraud risk, customer complaints, and regulatory trouble. That doesn't make the refusal acceptable, but it helps to understand what's driving it.

Document problems banks worry about

Some refusals happen because the documents themselves raise questions.

- Outdated papers: A power of attorney may be old, hard to read, or missing pages.

- Unclear authority: The wording may not clearly cover the transaction you're trying to complete.

- Capacity concerns: Staff may wonder whether the person understood the document when signing it.

- Institution-specific review: A branch may send the matter to an internal legal or risk team, even when the document appears facially valid.

If the issue involves guardianship, banks also look closely at whether your Letters of Guardianship are current and whether any bond, oath, or court condition affects your authority. In Texas guardianship practice, courts supervise guardians rather than issuing one paper and stepping away as their sole action. That supervision matters to banks.

The bank's compliance mindset

Texas banks also operate in a wider compliance environment. Refusal isn't always about your family. Sometimes it's about the bank trying to avoid making a verification mistake in a regulated setting.

Texas breach-notice rules require notice to affected individuals within 60 days of discovery, and incidents affecting 250 or more Texans must also be reported to the Attorney General within that same 60-day window, as described in Texas banking compliance guidance. If a bank can't confidently verify who has authority to act, that caution can spill into how it handles records access, remediation steps, and customer-facing decisions.

That doesn't mean the bank is right to block you. It means the bank may be reacting from fear of compounding a compliance problem.

Practical rule: The branch counter is often the wrong battlefield. The real decision maker may be the bank's legal, trust, or risk department.

Common real-world reasons for refusal

Here are the patterns families see most often:

| Reason | What it means in practice |

|---|---|

| Internal policy | The bank has a review process that frontline staff must follow |

| Fraud concern | Staff fear unauthorized access or elder exploitation |

| Incomplete file | The bank wants ID, certifications, or updated court papers |

| Mismatch | The name on the account, ID, or court document doesn't line up cleanly |

| Scope issue | Your document may authorize some acts, but not the exact act requested |

| Multi-party concern | Another family member disputes your role or has already contacted the bank |

If you understand the reason, you can usually choose a better response. If you don't, you'll waste time arguing with someone who may not have authority to fix it.

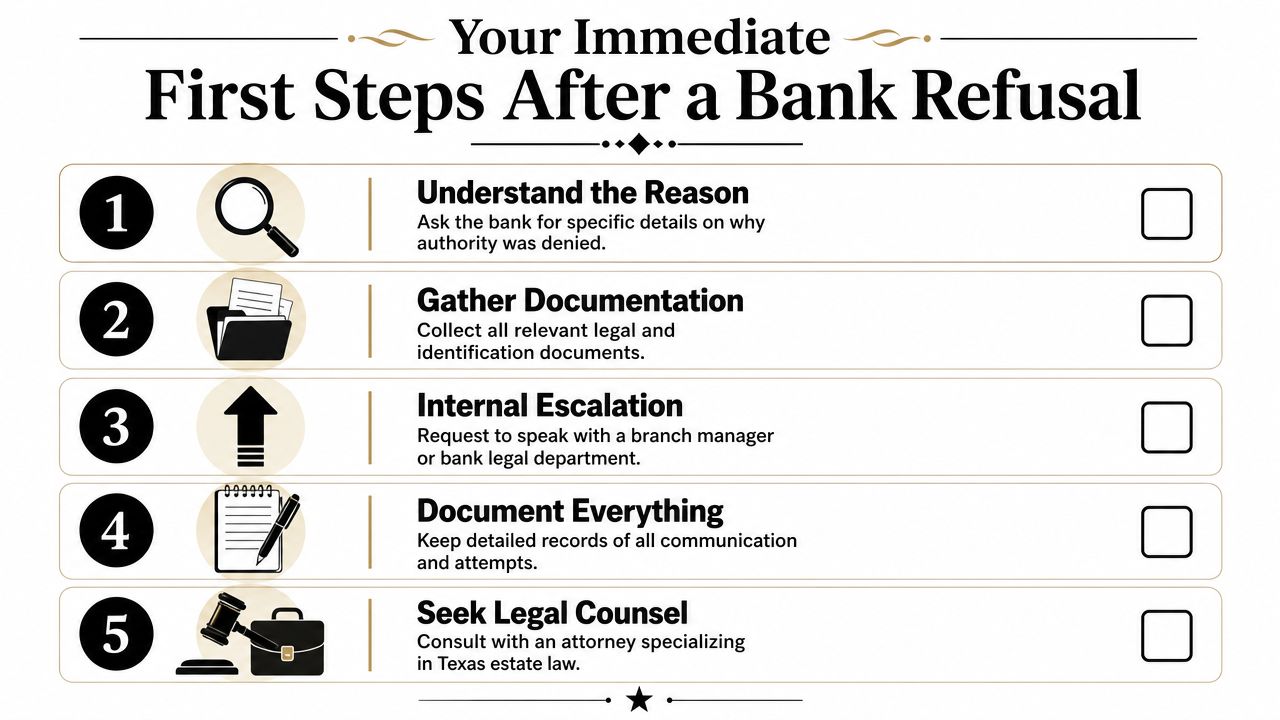

Your Immediate First Steps After a Refusal

The first few hours matter. The goal isn't to “win” at the teller line. The goal is to gather information, protect your position, and keep essential expenses from sliding into crisis.

Start by asking for the reason for refusal in plain terms. If the employee gives a vague answer, ask who made the decision and whether the refusal came from the branch, a manager, or a review department.

What to ask the bank before you leave

Use calm, specific questions.

- Ask for the exact reason in writing. If they won't give a letter on the spot, ask for an email or secure message.

- Ask what documents would satisfy the bank. Don't accept “we just can't.” Ask what is missing.

- Request escalation. A branch manager may still not control the outcome, but the file can often be moved upward.

- Write down names and times. Keep a simple log of who said what.

- Avoid withdrawing from your own funds to “fix it later” unless you've gotten legal advice. Reimbursement disputes can become ugly.

For families dealing with guardianship paperwork, it helps to review what Texas courts expect in proof and current authority. This guide on proof of guardianship in Texas is a useful starting point.

What to do about bills this week

The bank dispute may take time. Your loved one still has needs.

Consider these short-term moves:

- Call service providers early: Ask the facility, caregiver, pharmacy, or utility company for a brief hold, extension, or payment arrangement.

- Separate urgent from non-urgent expenses: Care, medication, housing, and insurance usually come first.

- Preserve every receipt: If a family member temporarily advances money, careful records matter.

- Don't mix funds casually: If you're acting for someone else, avoid informal transfers that blur whose money paid what.

Later in the process, many families also benefit from hearing a practical overview before speaking with counsel. This video can help frame the issue:

A simple script that works

You don't need to threaten anyone. Try this:

“I understand the bank needs to verify authority. Please tell me specifically what is missing, who is reviewing it, and what I need to provide so essential expenses for my family member can be paid.”

That language usually gets better results than anger. It tells the bank you expect a real answer and that you're building a record.

Formal Legal Remedies in Texas Probate Court

When internal escalation fails, the problem often shifts to probate court. In Texas, that may mean the statutory probate courts, county courts, or other courts with probate jurisdiction, depending on the county. In places like Harris County Probate Court, judges routinely handle disputes involving guardianship authority, estates, and control of property.

Guardianship authority under Texas law

If you are a guardian, your authority comes from court appointment, not from the bank's approval. Texas Estates Code Title 3, Subtitle G governs guardianship proceedings and ongoing administration. That includes applications, qualification, court supervision, duties, and compliance.

A few provisions matter especially in practice:

- Estates Code Chapter 1101: Covers guardianship applications.

- Estates Code Chapter 1201: Addresses temporary guardianship in urgent cases.

- Estates Code Chapter 1151: Covers powers and duties of a guardian.

- Estates Code Chapter 1163 and related compliance provisions: Deal with accountings and court oversight of estate management.

If the bank is blocking a duly appointed guardian from carrying out court-supervised duties, the probate court can become the place to force clarity.

Court tools that may solve the problem

The right remedy depends on where your authority comes from.

If you have guardianship papers, your attorney may ask the court for orders confirming your authority, directing a third party to honor it, or addressing interference with estate administration.

If your authority comes from a power of attorney, litigation may involve asking a court to determine validity, scope, or enforceability. Families often refer to this generally as seeking a court order that confirms the bank must recognize the document.

If probate is involved after death, the personal representative may seek relief tied to the estate's right to collect and manage assets.

Here's how that plays out in real life. Suppose a daughter in Houston needs access to funds for her father's immediate care. The bank won't honor the presented authority, and internal review is going nowhere. If she's already the court-appointed guardian of the estate, a lawyer can ask the probate court for targeted relief based on the existing guardianship case. If no guardianship exists and the father lacks capacity, the family may need to file for guardianship and, if the need is urgent, consider temporary relief under Chapter 1201.

If your loved one can't wait for a routine timeline, temporary guardianship may be the difference between delay and action.

Emergency and temporary relief

Temporary guardianship exists for situations where a person or estate faces immediate risk. In a bank-refusal setting, that might matter when funds are needed for housing, medication, or protection of assets. A temporary guardianship case still requires proof and court involvement, but it can provide a faster legal path than waiting through a prolonged informal dispute.

Families sometimes ask whether a strong demand letter is enough. Sometimes it is. Sometimes it isn't. A bank may change course once counsel frames the issue clearly and provides cleaner authority documents. Other times, only a signed order from a Texas judge moves the file.

For broader perspective on how financial-institution disputes can turn into litigation strategy questions, this guide on navigating legal battles with banks is useful as a general comparison point, even though Texas probate procedure is its own system.

Why administrative enforcement matters

Texas also gives bank regulators meaningful enforcement tools. In 2023, H.B. 3574 amended Texas Finance Code Section 35.002 so the banking commissioner may issue a cease-and-desist order not only to current bank officers, employees, or directors, but also to former ones, and Supervisory Memorandum 1005 was updated to reflect that change, as discussed in Texas banking legal updates. That same memorandum states that if certain bank participants refuse to comply with a subpoena under Section 31.105, the commissioner may issue an emergency removal order barring participation in the affairs of the bank or another regulated entity until compliance occurs.

For families, the takeaway is simple. Texas banking regulation is not casual. When a bank mishandles legal authority issues, the consequences can move beyond a customer-service dispute. That often gives added weight to a carefully prepared legal challenge.

Comparing Your Options Timelines Costs and Risks

Families usually want one answer. In reality, there are several paths, and each carries trade-offs. The right choice depends on urgency, the quality of your documents, whether incapacity is disputed, and how much cooperation you're getting from the bank.

Comparing remedies for bank refusal

| Remedy | Timeline | Cost | Best For |

|---|---|---|---|

| Informal branch follow-up | Usually the fastest if the problem is a missing item | Usually the lowest direct cost | Simple document issues or staff misunderstanding |

| Internal bank escalation | Often slower than families expect, but still less disruptive than court | Moderate, especially if an attorney prepares a focused demand | Cases where authority is valid but the file needs legal review |

| Probate court action | Often the most demanding path | Higher because filings, preparation, and hearings may be required | Urgent care needs, disputed authority, or repeated refusal |

| Temporary guardianship or emergency relief | Used when delay threatens the person or estate | Higher and fact-specific | Immediate risk to health, safety, or finances |

Here, practical judgment matters. If the document problem is fixable, litigation may be unnecessary. If the bank has already dug in and your loved one's care is at risk, waiting too long can cost more than moving quickly.

What works and what usually doesn't

What works:

- A clean document packet

- A short, precise written explanation

- Escalating to the correct internal department

- A lawyer who understands guardianship, probate, and fiduciary duties

What usually doesn't:

- Repeated branch visits with no new information

- Angry demands without a paper trail

- Paying major expenses from mixed family funds and sorting it out later

- Assuming a valid document will “speak for itself”

If your authority issue centers on a power of attorney, it helps to compare your paperwork against Texas-specific expectations. This overview of the Texas power of attorney form can help you spot common issues before deciding whether to escalate.

For families trying to understand how probate timing can vary by state and court system, this article on the probate process in Utah is a helpful contrast. It isn't Texas law, but it shows why broad internet advice about “how long probate takes” often misses local court realities.

The cheapest option at the start isn't always the least expensive overall. Delay can create late fees, care interruptions, and avoidable court fights.

How to Prevent Bank Refusals Before They Happen

The cleanest solution is prevention. Most families won't avoid every problem, but they can sharply reduce the chance of a damaging refusal.

Build a bank-ready file

If you're using a power of attorney, the document should be properly executed, clear, and easy for a bank reviewer to follow. If a guardianship is likely in the future, don't wait until a medical crisis to learn how estate management and court authority work.

A practical prevention plan usually includes:

- Choose familiar forms when appropriate: Banks are more comfortable with documents they regularly review.

- Avoid unclear custom language: Complex drafting can create unnecessary review problems.

- Keep certified or current copies available: Don't rely on a faded scan in an email chain.

- Match names carefully: The name on the ID, account, and legal document should line up.

- Introduce the agent early if possible: It helps when the bank has seen the relationship before a crisis.

Think beyond the document itself

Good planning also means choosing the right legal tool. Not every family needs guardianship. Some situations can be handled through estate planning, a power of attorney, supported decision-making, or account structuring done in advance. Other situations require court supervision because the person is already incapacitated, conflict is present, or financial protection needs are serious.

If your family is planning ahead for court oversight of finances, this guide to Texas guardianship bank account rules explains issues that often cause trouble later.

For some families, it also helps to coordinate planning across related areas instead of handling each problem separately. That may include guardianship analysis, estate planning, and probate preparation with one legal team. Law Office of Bryan Fagan, PLLC handles those categories of work in Texas, which can be useful when authority disputes overlap with larger family or court issues.

When You Need a Texas Guardianship and Probate Attorney

Some bank disputes can be solved with persistence and better paperwork. Others need legal intervention quickly.

You should strongly consider hiring a Texas guardianship and probate attorney if any of these are true:

- The bank won't state the reason for refusal in writing

- Care, housing, or medical expenses are immediately at risk

- Another relative is challenging your authority

- The person may need guardianship, not just a power of attorney

- The bank keeps pushing the issue through “review” with no clear resolution

- You may need court orders, temporary guardianship, or probate litigation

A lawyer's role isn't limited to filing suit. Sometimes counsel resolves the matter by presenting the right records, contacting the bank's legal department, and framing the issue as a fiduciary or probate matter that needs prompt handling. In more serious cases, counsel can prepare a guardianship application, seek temporary relief, or ask the probate court to enter enforceable orders.

If you're dealing with what happens when a bank refuses to recognize your authority in Texas, don't wait until missed payments and family conflict make the problem harder to fix. Early legal advice often protects both the vulnerable person and the family member trying to help.

If your family is facing a bank refusal tied to a power of attorney, guardianship, probate, or estate administration, Law Office of Bryan Fagan, PLLC can help you assess your options and build a practical plan for both the legal dispute and the immediate cash-flow problem. We assist families across Texas, including matters involving Houston, Dallas, Austin, San Antonio, and surrounding counties. Schedule a free consultation to get guidance suited to your documents, your court, and your loved one's urgent needs.