Skip to content

Skip to contentWhen you are thinking about the future and protecting your family, the legal jargon can feel overwhelming. But there’s one tool designed specifically to make things simpler for your loved ones: the non-probate asset. In simple terms, a non-probate asset is property that transfers directly to a specific person when you pass away, completely bypassing the lengthy and very public probate court process.

Think of it as a direct path for your assets. It goes straight to your loved ones without them having to wait in the long, slow-moving line at the courthouse, a process that can add stress during an already emotional time.

Understanding the Non-Probate Asset in Texas Estate Planning

After a loved one passes, their estate often has to go through a court-supervised process called probate. This is where a court validates the will, makes sure debts are paid, and then legally distributes whatever property is left. While it's a necessary step for some assets, probate can be time-consuming, expensive, and everything becomes public record.

A non-probate asset, however, gets to skip all of that.

The magic behind this shortcut isn't magic at all—it’s simple contract law. When you set up an account and name a beneficiary, you're creating a legal contract. That contract dictates exactly who receives the asset upon your death, and it legally overrides whatever your will might say about that specific property.

How Non-Probate Transfers Work

This direct-transfer mechanism offers families a huge amount of emotional and financial relief during what is already an incredibly difficult time. Let’s break down the core benefits:

- Speed: Beneficiaries can often access funds within weeks, not the months or even years probate can drag on. This immediate access can be critical for covering funeral costs or day-to-day living expenses.

- Privacy: Probate is a public court proceeding, meaning anyone can look up the details of the estate. Non-probate transfers are private transactions between the financial institution and the beneficiary, keeping your family’s affairs out of the public eye.

- Cost Savings: By sidestepping the court, you also sidestep court fees, certain attorney costs, and other administrative expenses tied to the probate process. This means more of the asset's value goes directly to your loved ones.

Under the Texas Estates Code, Title 3, probate is the default path for many assets. But a properly designated non-probate asset operates under contract law. This allows it to pass directly to a beneficiary and give your family faster, more private access to much-needed resources.

A classic example is a life insurance policy. You name your spouse as the beneficiary, and upon your passing, the insurance company is contractually obligated to pay the proceeds directly to them. The Harris County Probate Court has no say in that transaction. This same principle works for retirement accounts, certain bank accounts, and any assets held inside a living trust.

To help you see the difference more clearly, let's compare how these two types of asset transfers work in the real world.

Probate vs. Non-Probate Asset Transfers in Texas

| Transfer Characteristic | Probate Assets (e.g., a solely owned house with a will) | Non-Probate Assets (e.g., a life insurance policy) |

|---|---|---|

| Transfer Process | Requires court validation of the will. An executor is appointed to manage the estate, pay debts, and distribute assets. | Transfers directly to the named beneficiary upon presentation of a death certificate. No court involvement needed. |

| Speed of Transfer | Can take 6 months to over a year, sometimes longer if the will is contested or the estate is complex. | Typically takes just a few weeks. Beneficiaries get access to funds quickly. |

| Privacy Level | Public record. The will, asset inventory, and distribution details are filed with the court and accessible to anyone. | Completely private. The transfer is a confidential transaction between the financial institution and the beneficiary. |

| Associated Costs | Incurs court filing fees, executor fees, appraiser fees, and often significant attorney's fees. | Minimal to no costs. Usually just requires some simple paperwork. No court or legal fees are necessary for the transfer itself. |

| Control | The will dictates distribution, but the process is controlled and supervised by the probate court. | The owner has complete control through the beneficiary designation, which overrides the will. |

As you can see, the differences are stark. Relying solely on a will means your family will likely face a public, expensive, and slow process for those assets. Integrating non-probate assets creates a much smoother, more efficient path for your beneficiaries.

Understanding this foundational concept is the first step toward building a truly protective and thoughtful estate planning strategy. At The Law Office of Bryan Fagan, we specialize in helping Texas families navigate these details with clarity and care. Schedule a free consultation with us today to discuss how to best protect your legacy.

Common Types of Non-Probate Assets for Texas Families

So, you understand the big idea: some of your assets can skip the court process. Now, let's dig into the most common types of non-probate assets that many Texas families already have, often without even realizing their estate planning power.

These aren't complicated legal loopholes; they're straightforward tools designed for privacy and efficiency. Each one lets you leave clear, simple instructions for passing your legacy directly to your loved ones. While they all operate under slightly different rules, the goal is always the same: a smoother, faster transfer when the time comes.

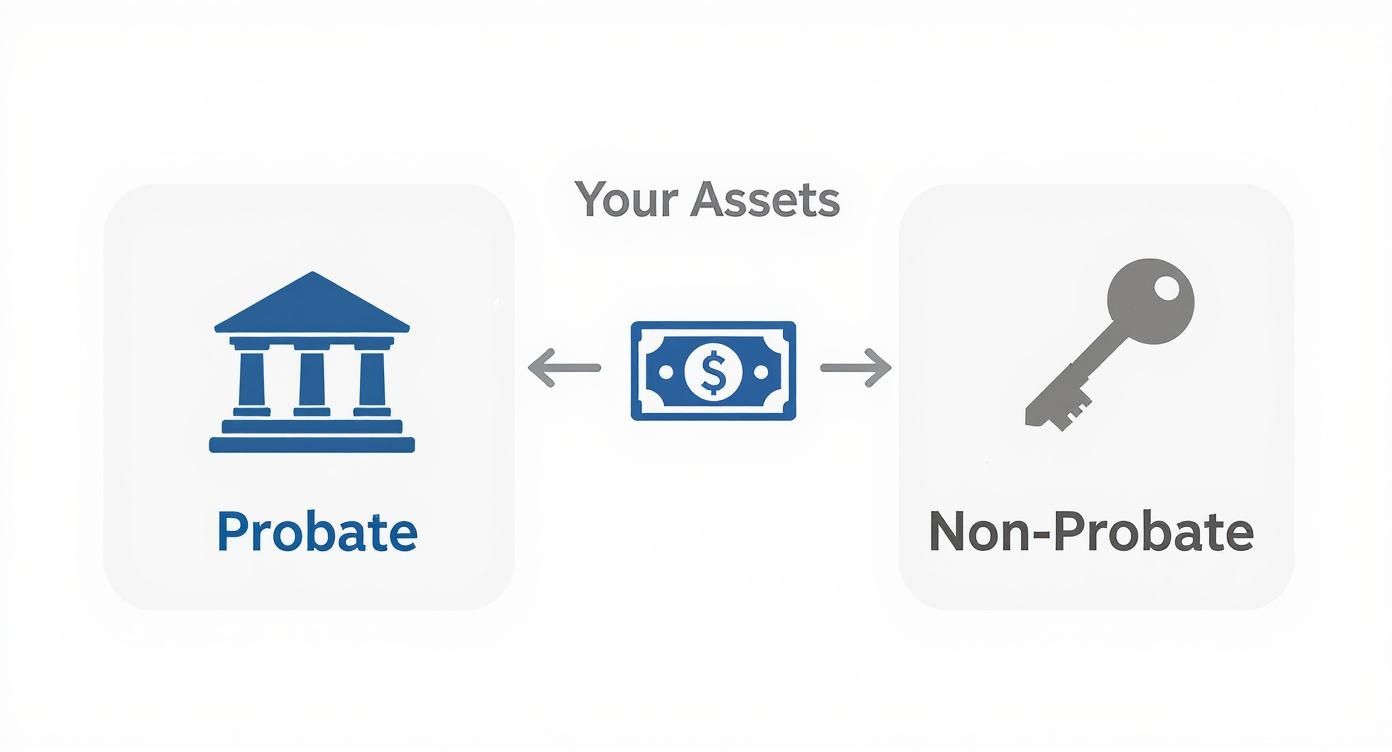

This picture helps visualize how assets get split between the probate path (the courthouse) and the non-probate path (the key).

As you can see, while some assets absolutely must go through the formal court system, many can be passed directly to your heirs if you use the right legal tools ahead of time.

Property Owned Jointly with Right of Survivorship

Many married couples in Texas own their home as joint tenants with right of survivorship (often abbreviated as JTWROS). This is a powerful and common form of co-ownership that provides peace of mind.

When one owner passes away, their share automatically—and immediately—transfers to the surviving owner. It completely bypasses probate. For example, if a husband and wife in Harris County own their home this way, the surviving spouse becomes the sole owner with just a bit of simple paperwork. The same principle works for joint bank or investment accounts marked with "JTWROS." It's an incredibly effective strategy for couples.

You might also hear about other deed types that offer similar benefits, like a Lady Bird Deed, which you can read more about in our other articles.

Accounts with Beneficiary Designations

This is probably the most common category of non-probate asset. It covers any account where you have a contract that lets you name a specific person to inherit the funds when you pass away.

- Payable-on-Death (POD) Accounts: These are your standard bank accounts, like checking or savings. You fill out a simple form at the bank to name your beneficiary. When you pass away, that person just needs to show the bank a death certificate to claim the funds.

- Transfer-on-Death (TOD) Accounts: This works exactly like a POD account, but it’s for investment and brokerage accounts holding stocks, bonds, or mutual funds.

- Life Insurance Policies: The death benefit from a life insurance policy is paid directly to the beneficiaries you named in the policy. It never touches the probate court.

- Retirement Accounts (401(k)s, IRAs): These accounts are also transferred directly to your designated beneficiaries, steering clear of the delays and costs of probate.

Assets Held in a Living Trust

A living trust is a legal tool you create to hold the title to your most valuable assets—think your house, investments, or bank accounts. During your lifetime, you control everything as the trustee.

When you pass away, a successor trustee you've already chosen steps in. Their job is to distribute the assets to your beneficiaries exactly as you instructed in the trust document, all without any court supervision.

Even though trusts are incredibly effective, a surprising number of people haven't set one up. In fact, research from IBISWorld projects that by 2025, only 13% of Americans will have a living trust—a key tool for avoiding probate.

Knowing which of your assets are non-probate is the foundation of a solid estate plan. If you need a hand identifying and managing these assets, schedule a free consultation with The Law Office of Bryan Fagan.

How These Assets Bypass the Texas Probate Process

So, why do some of your assets get a free pass around the Texas probate system while others have to go through the whole court process? The secret isn't some complex legal loophole. It's actually much simpler: contract law.

When you set up certain accounts or policies, you enter into a binding agreement with a financial institution—think a bank, an insurance company, or an investment firm. As part of that deal, you fill out a form naming a specific person or people as your beneficiaries. This is the person who will receive that asset when you pass away.

That signed beneficiary form is a legally binding contract. It legally supersedes any instructions you might have left in your will. Because the transfer is dictated by this pre-existing agreement, it doesn't need a judge's approval to happen.

The Power of a Contract

Here's an easy way to think about it: your will is a set of instructions for the probate court, but a beneficiary designation is a direct order to a financial company. The Texas Estates Code governs what happens inside a probate courtroom, but these direct orders are handled completely outside of it.

This contractual shortcut creates a streamlined path for your assets to get to your family, delivering three powerful benefits during what is already a very difficult time.

- Speed: Funds are often available within weeks, not the months or even years that probate can take.

- Privacy: The transfer is a confidential matter between your beneficiary and the financial institution, not a public court record for anyone to see.

- Cost Savings: Skipping the court process means avoiding court fees and many of the legal expenses that come with probate.

A classic, compassionate example of this is a Payable-on-Death (POD) bank account right here in Fort Bend County. A grieving family can simply present a death certificate to the bank and access those funds almost immediately to cover funeral expenses. They get to bypass the stressful delays and costs of probate court entirely.

The Bigger Picture in Wealth Transfer

This method of transferring wealth isn't just a minor detail in estate planning; it's absolutely central to how inheritances are passed down today. The use of non-probate assets is a massive and growing part of wealth transfers across the globe.

In fact, projections show that by 2048, American retirees are expected to transfer over USD 124 trillion to their heirs and charities. The vast majority of this staggering sum will flow through non-probate tools like trusts and beneficiary designations, avoiding direct court involvement. You can dig deeper into these trends and their impact on global wealth planning.

Understanding the power of these contracts is the key to smart estate planning. It allows you to build a financial safety net that provides for your family efficiently, privately, and with far less stress. Our team at The Law Office of Bryan Fagan is dedicated to helping Texas families use these tools effectively. For personalized guidance on structuring your assets to protect your loved ones, we invite you to schedule a free consultation.

The Critical Importance of Managing Beneficiary Designations

Of all the challenges we see families face in estate planning, one simple mistake causes the most heartbreak: the outdated beneficiary designation. A non probate asset transfers based on the name on that form, and that designation is a binding contract. It overrides everything else—including your will.

This isn't a minor detail; it's the final word on where your hard-earned assets will go.

We’ve seen this play out in a tragic, and all-too-common, scenario. A person names their spouse on a 401(k) beneficiary form early in their career. Years later, they divorce and remarry, building a new life and family. They go to the trouble of updating their will to leave everything to their new spouse and children but completely forget to change that one form from decades ago.

When they pass away, the entire 401(k)—often the largest single asset they own—legally belongs to the ex-spouse. Their current family is unintentionally disinherited from that account. There is absolutely nothing the will or the probate court can do to fix it. That beneficiary form is a contract, and the contract is the final word.

Why This Oversight Is So Dangerous

This issue is far more common than people realize. Because non-probate assets operate independently of a will, they create a unique risk. A shocking number of people simply don't update these forms after major life changes. This oversight can lead to assets transferring to former spouses or other unintended heirs, completely derailing a carefully crafted estate plan. To get a sense of how these designations are handled globally, you can explore detailed insights on worldwide estate and inheritance tax guidance.

The single most powerful step you can take to protect your family is to regularly review every beneficiary designation you have. It costs nothing but can save your loved ones from immense financial and emotional pain.

A Practical Checklist for Your Beneficiary Forms

To prevent this from happening to your family, you need to treat your beneficiary designations with the same importance as your will. Set a calendar reminder to review them once a year and, more importantly, update them immediately after any significant life event.

Use this checklist to stay on track:

- Marriage: Add your new spouse to the relevant accounts.

- Divorce: Remove your former spouse immediately. A divorce decree does not automatically update these forms for you.

- Birth or Adoption of a Child: Make sure your children are included as primary or contingent (backup) beneficiaries.

- Death of a Beneficiary: If a named beneficiary passes away, you must name a new one. If you don't, the asset could end up back in your probate estate anyway.

- Minor Children Turning 18: When your kids become adults, you may want to update designations to name them directly instead of through a custodian.

This simple review is one of the most loving and protective actions you can take for your family. If you're unsure where to start or need help aligning your designations with your overall estate goals, The Law Office of Bryan Fagan offers a free consultation to guide you.

Integrating Non Probate Assets Into Your Complete Estate Plan

It’s easy to think of non-probate assets as a magic bullet for estate planning—and while they are powerful tools for efficiency and privacy, they’re just one piece of a much larger puzzle. A truly protective estate plan is one where all your legal documents work together in harmony. If you rely only on beneficiary designations, you could be leaving your family vulnerable to some dangerous gaps.

For example, your will is the only legal document where you can name a guardian for your minor children. If you were to pass away unexpectedly, a POD account could get money to a loved one quickly, but it can’t do a thing to protect your kids’ future. A comprehensive plan, on the other hand, coordinates your will, powers of attorney, and non-probate assets into a single, unified strategy that covers all the bases.

Creating a Cohesive Strategy

Think of your estate plan like a team where each player has a specific job. Your will handles probate assets and names guardians. Your durable power of attorney lets someone make financial decisions if you become incapacitated. Your non-probate assets ensure a fast transfer of key funds. If these players aren’t working from the same playbook, they could end up working against each other.

The goal is to build a complete safety net for your family’s future, not just a collection of separate documents. A well-integrated plan ensures there are no conflicts or unintended consequences that could harm your loved ones.

At The Law Office of Bryan Fagan, we specialize in helping Texas families create this kind of cohesive plan. We make sure every document supports the others, from the beneficiary designations on your IRA to the guardianship provisions in your will. This comprehensive approach is absolutely crucial for protecting your family from every angle. A key part of integrated planning is considering alternatives to guardianship, which can often be addressed through robust powers of attorney and trusts, preserving autonomy and reducing court involvement.

Tools to Support Your Plan

Building a truly comprehensive estate plan means drafting multiple, interlocking documents. While resources like templates for legal documents for personal needs can be a good starting point for getting organized, they come with a major caveat. These tools should always be used under the guidance of a qualified attorney to ensure they align perfectly with Texas law and your unique family situation.

Your family’s security is far too important to leave to chance or guesswork. Let us help you build a plan where every single piece fits together perfectly. Schedule a free consultation with our team today to get started.

How a Guardianship Can Affect Non Probate Assets

When someone becomes incapacitated and a guardian is appointed, it can create challenges for even the most carefully laid plans. Families in Texas often find themselves navigating this tough situation, worried about how their loved one's assets—especially non-probate ones—will be handled.

If a Montgomery County court appoints a guardian of the estate under Texas Estates Code, Title 3, Subtitle G, that person gains the legal authority to manage the incapacitated person's financial life. This isn't just about paying bills; it involves overseeing everything from bank accounts to investments to ensure the person's needs are covered.

But a guardian's power isn't a blank check. There are firm limits, particularly when it comes to changing the final destination of a non-probate asset.

A Guardian's Limited Authority

A guardian can't just wake up one day and decide to change the beneficiaries on a life insurance policy or a 401(k). The Texas Estates Code is very clear on this. Altering a beneficiary designation is a major decision that requires explicit permission from a judge after a formal hearing.

Judges are very hesitant to approve these kinds of changes. Why? Because it directly contradicts the wishes the original owner put in place when they were of sound mind. This legal safeguard is there for a reason: to protect the integrity of your estate plan and honor your loved one's intentions. You can learn more about the specifics in our guide on how guardianship impacts life insurance policies in Texas.

For a broader perspective on the guardianship process, it can also be useful to review information on topics like how to get temporary guardianship without court to see how different legal avenues work.

A Practical Scenario in Guardianship

Let's walk through a common example. Picture an elderly man in The Woodlands who set up a large TOD investment account to go directly to his three children upon his death. Unfortunately, he develops dementia, and the court appoints his daughter as his guardian. As his medical bills pile up, she needs a way to pay for his long-term care.

- What she can do (Practical Steps): The guardian can petition the court for permission to sell some of the investments in that TOD account to cover her father's necessary expenses. The court will almost certainly grant this, as it's for his direct care and well-being. This involves filing the correct motions and providing evidence of the need.

- What she can't do: She cannot, on her own authority, remove her siblings as beneficiaries and name only herself. Getting a court order for that would be an uphill battle, and for good reason. Guardians have a duty to act in the best interest of the person they serve, not to alter their established estate plan.

This is exactly why proactive planning is so crucial. A well-drafted durable power of attorney can often serve as an alternative to a court-supervised guardianship entirely. It allows the person you choose (your agent) to manage your affairs without having to constantly seek a judge's approval.

If your family is facing these complex challenges, don't go it alone. Schedule a free consultation with The Law Office of Bryan Fagan for compassionate, straightforward guidance.

Frequently Asked Questions About Texas Non-Probate Assets

When you start digging into the details of estate planning, a lot of specific questions tend to pop up. To help clear up some common points of confusion, we've put together straightforward answers to the questions we hear most often from Texas families.

Does a Will Override a Beneficiary Designation in Texas?

No, it absolutely does not. This is a critical point that trips up many people. A beneficiary designation on any account—be it a life insurance policy, a 401(k), or a bank account—is a binding legal contract. That contract always takes precedence over whatever your will says.

Think of it this way: if your will clearly states that your children inherit everything, but your IRA still lists your ex-spouse as the beneficiary, that IRA is going to your ex-spouse. Period. This is precisely why reviewing and updating your beneficiary designations regularly is one of the most important things you can do for your estate plan.

Are Non-Probate Assets Subject to Creditor Claims?

This is another one of those "it depends" situations. Under Texas law, certain non-probate assets get strong protection from creditors. Life insurance proceeds and retirement accounts, for example, are generally shielded and can pass to your beneficiaries without being intercepted to pay your debts.

However, other assets aren't so lucky. Funds in a Payable on Death (POD) bank account might still be reachable by creditors to settle any outstanding debts your estate owes. An experienced estate planning attorney can look at your specific assets and tell you exactly what's protected and what's not.

What Happens If My Named Beneficiary Dies Before Me?

This is a scenario that can completely derail your plans if you're not prepared. If you don't name a contingent (or secondary) beneficiary and your primary beneficiary passes away before you do, the asset often loses its non-probate status.

When that happens, the asset gets kicked back into your probate estate. It will then be distributed according to the terms of your will or, if you don't have one, Texas intestacy laws. This unfortunately defeats the entire purpose of setting it up to avoid probate in the first place and can cause significant delays and complications for your family.

Navigating the complexities of non-probate assets and weaving them into a cohesive estate planning strategy is a critical step in protecting your family’s future. For personalized guidance tailored to your unique situation, contact The Law Office of Bryan Fagan, PLLC today. Schedule a free, no-obligation consultation by visiting https://texasguardianshiplawyer.net to ensure your legacy is secure.