Skip to content

Skip to content You open a drawer looking for a Medicare card and find something else instead. Unopened bills. A credit card statement that doesn’t make sense. A bank alert on your parent’s phone for a withdrawal they can’t explain. In that moment, most families don’t think, “I need legal authority.” They think, “How do I protect Mom without humiliating her?”

That instinct is right. In Texas, taking control of an elderly parent’s finances legally is not about grabbing power. It’s about using the right legal tool at the right time, with the least loss of independence possible. Sometimes that means a signed power of attorney. Sometimes it means a trust. Sometimes it means asking a probate court in Harris County, Fort Bend County, or another Texas county to appoint a guardian because there is no safe alternative left.

The hard part is that families usually arrive here under stress. A parent may be grieving, sick, suspicious, or embarrassed. Siblings may disagree. A bank may refuse to honor paperwork. And if no planning was done early, the law gets more formal very quickly. That’s where clarity matters.

Recognizing the Need for Financial Help

The warning signs often start small. A parent who always paid bills on time begins missing due dates. They donate repeatedly to the same caller. They insist everything is fine, but utilities are overdue and check registers no longer match account balances. Some families discover the problem only after a scam, a hospitalization, or a notice that property taxes were not paid.

In Texas, delay can be costly. In 2021 alone, Texans who were victims of elder fraud lost $159,614,547, according to Texas Appleseed’s reporting on senior financial abuse. That figure covers reported fraud only. It does not capture every case where a caregiver, relative, or other trusted person drains an older adult’s money.

What families usually notice first

The first clues are rarely legal. They’re practical.

- Bills stop getting paid: Mortgage, rent, insurance, or utilities begin slipping.

- Unusual withdrawals appear: Cash withdrawals, wire transfers, or gift card purchases don’t fit your parent’s habits.

- Mail piles up: Statements, collection notices, and renewal forms go unopened.

- Basic money tasks become confusing: Your parent mixes up account balances, forgets automatic drafts, or can’t explain recent charges.

- A new “friend” gets involved: Someone suddenly has strong influence over spending or banking access.

Practical rule: Treat repeated financial confusion as a safety issue, not a personality issue.

Protection is the goal, not control

Many adult children feel guilty even asking whether they should step in. That guilt is normal, but it can keep families frozen. The better frame is this: if your parent can no longer manage money safely, doing nothing is also a decision. It leaves them exposed to scammers, late fees, lapses in care, and family conflict.

Texas law gives families structured ways to help. The two most common paths are a Durable Power of Attorney when a parent still has capacity, and guardianship when they no longer do. Those are very different tools. One is private planning. The other is court supervision.

If your parent is already resisting help, a practical starting point is learning what to do when a parent refuses help but clearly needs it in Texas. Resistance doesn’t always mean stubbornness. Often it means fear.

When concern becomes urgency

Some situations can’t wait for a family meeting next month.

- Accounts are actively being drained

- A caregiver or relative is isolating the parent

- Your parent is signing documents they don’t understand

- Essential bills or care costs are at risk

- There’s evidence of a scam in progress

When those facts are present, families need legal advice quickly. Informal help, shared passwords, and verbal permission may feel easier in the moment, but they often fail exactly when pressure rises.

Assessing Capacity and Starting the Conversation

A daughter in Sugar Land notices her father has paid the same roofing company twice, even though no work was done. He laughs it off and says he’s “just tired.” Two weeks later, he can’t explain why he withdrew cash three days in a row. He still knows his children’s names, still drives to breakfast, and still insists he handles his own affairs. Families often get stuck in this situation. They see decline, but not total collapse.

Texas law does not require a person to be bedridden or completely disoriented before financial help becomes necessary. The fundamental question is whether the parent can understand and manage the decisions in front of them. Capacity is task-specific in many real-life situations. A parent may be able to choose lunch and still be unable to evaluate a bank transfer, a refinance offer, or a sweepstakes scam.

Signs that financial capacity may be slipping

Watch behavior over time, not one bad day.

- Repeated confusion about routine money tasks: forgetting due dates, misreading balances, duplicating payments

- Poor judgment with strangers: sending money to callers, online contacts, or “charities” without clear reason

- Loss of paperwork control: hidden statements, unsigned checks, missing tax records

- Abrupt changes in spending patterns: large gifts, unusual subscriptions, or withdrawals with no explanation

- Defensiveness tied to obvious mistakes: anger that masks confusion, especially when you ask simple questions

A medical diagnosis like dementia matters, but families often notice the money problems before a formal diagnosis exists.

How to start without making it a fight

The opening line matters. If your parent hears, “You can’t handle your finances anymore,” the conversation usually ends there. If they hear, “I want to make this easier and safer for you,” they’re more likely to stay in it.

Try language like this:

“I’m not trying to take anything away from you. I want to help make sure the bills are paid the way you want and that nobody takes advantage of you.”

Or this:

“Would it help if we sat down together and made a list of your accounts and automatic payments, just so there’s a backup if you’re sick or in the hospital?”

Those openings preserve dignity. They also focus on planning instead of blame.

A simple approach that works better than arguing

Use a three-part conversation.

- Start with one concern, not ten. Pick a specific issue, like a missed insurance payment.

- Offer help in a limited way. Suggest organizing statements or attending one bank meeting together.

- Ask for their preferences. Who would they trust to help if they were temporarily unable to act?

That last question is often the doorway to a power of attorney.

Here’s what usually doesn’t work:

- Cornering a parent in front of siblings

- Using words like incompetent or unfit

- Threatening guardianship at the first meeting

- Taking over accounts without authority

- Mixing old family grievances into a present safety issue

When a parent says no

A refusal doesn’t always end the matter. It tells you what problem you’re dealing with.

| Parent’s response | What it may mean | Better next move |

|---|---|---|

| “I’m fine.” | Fear of losing independence | Offer a limited review of bills together |

| “You just want my money.” | Mistrust or family history | Bring in a neutral attorney or advisor |

| “Later.” | Avoidance | Set a specific date and narrow the task |

| “I already handled it.” | Confusion or denial | Ask to see the document or account record |

If your parent still has capacity, the law favors voluntary planning. If they don’t, the conversation may shift from persuasion to protection.

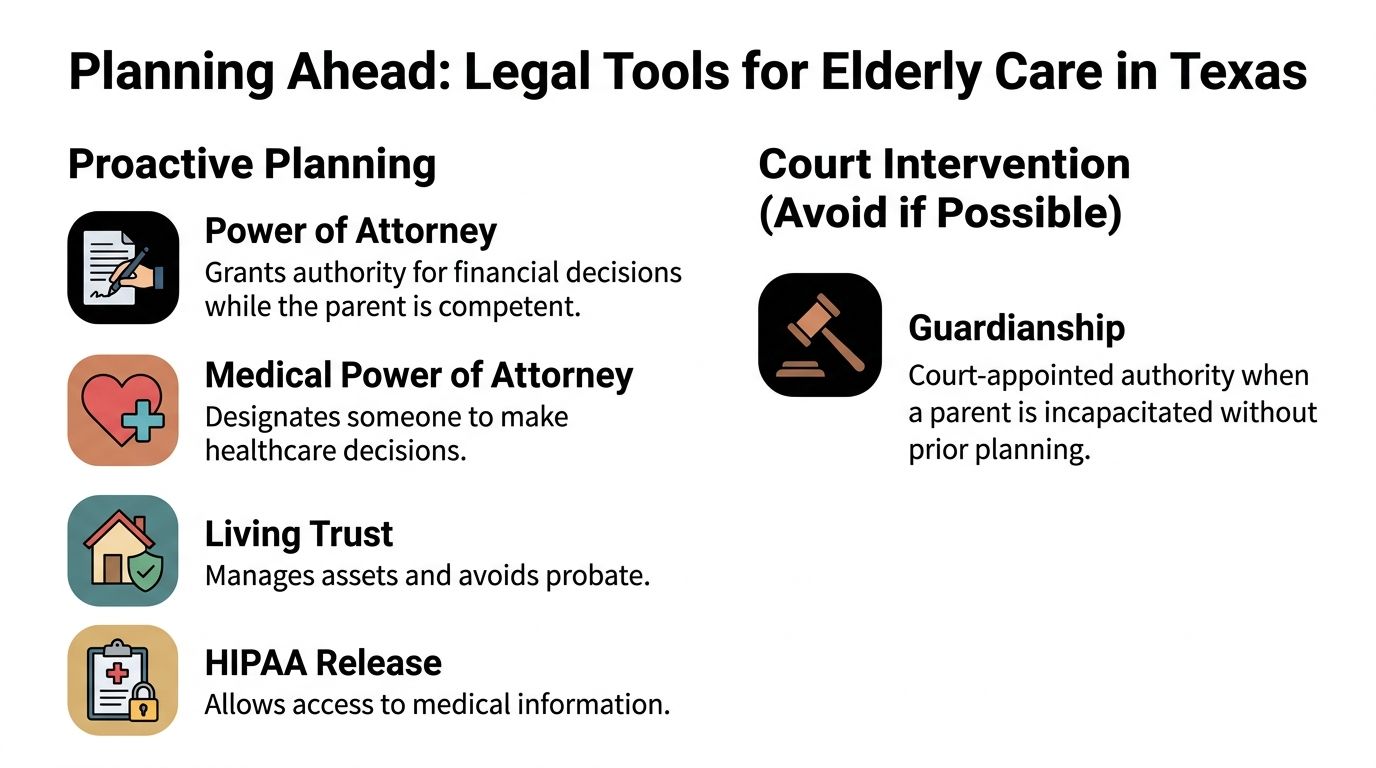

Proactive Tools The Power of Attorney and Other Alternatives

A common turning point looks like this. Your mother agrees she needs help paying bills after a hospital stay, but she still wants control. That is often the right moment to put legal authority in place, before a bank freeze, missed tax payment, or family dispute turns a manageable problem into a court case.

For financial decisions, the document families use most often is a Durable Power of Attorney, or DPOA. If the parent still has capacity, a DPOA usually gives the family the fastest and least restrictive way to act. It lets the parent choose who will help, define what that person can do, and avoid asking a judge for authority that could have been granted privately.

Families who want a closer look at how this works can read more about power of attorney over a parent in Texas and what authority the document can and cannot grant.

What a Durable Power of Attorney does

Under Texas law, the principal signs the DPOA before a notary and names an agent to handle financial matters. The word durable matters. It means the authority continues even if the parent later becomes incapacitated, assuming the document was validly signed in the first place.

A well-drafted DPOA can authorize the agent to handle:

- Bank accounts and bill payment

- Investment and brokerage accounts

- Credit cards and recurring expenses

- Insurance matters

- Tax filings and related paperwork

- Real estate transactions, if the document supports them and recording is handled where needed

- Gifting or trust-related powers, but only if the language clearly grants them

Some DPOAs take effect as soon as they are signed. Others are springing and only become effective after incapacity under the terms of the document. In practice, I often tell families to think carefully before choosing a springing form. It can sound safer, but it sometimes creates delay at the exact moment quick action is needed, especially if the bank wants proof of incapacity in a form no one anticipated.

The practical problems families run into

A signed DPOA is not self-enforcing. Banks review the document line by line. If the form is old, vague, missing required powers, or inconsistent with the institution's internal procedures, the agent may still hear no at the teller line.

That does not always mean the bank is right. It means the family needs a next move.

Start by asking for the reason in writing. Ask whether the problem is the age of the document, missing initials on certain powers, lack of a certification from the agent, or a request for the bank's own affidavit form. Escalate the issue to the branch manager or legal department. If the parent still has capacity, the cleanest fix may be signing an updated DPOA and delivering it before the account is needed for an urgent transaction.

If the parent is homebound but still capable, execution logistics matter. A convenient notary for Sugar Land can make it easier to get the document signed correctly without another draining trip across town.

Other tools that may help, and their trade-offs

A DPOA is usually the main financial tool, but it is rarely the only one worth discussing. The right mix depends on the assets, the family dynamic, and whether the parent wants one helper or a more structured arrangement.

| Tool | Good use | Main risk |

|---|---|---|

| Durable Power of Attorney | Day-to-day financial management without court involvement | A weak form may be rejected or may not cover the needed transaction |

| Joint bank account | Short-term bill paying access | The co-owner may be treated as an owner, which creates inheritance and misuse problems |

| Revocable living trust | Managing titled assets through a trustee | It only helps with assets actually transferred into the trust |

| Supported decision-making agreement | Helping a parent understand and communicate choices | It does not give direct control over accounts |

| Informal password sharing | Temporary access in an emergency | It gives no legal authority and creates serious abuse and fraud concerns |

Joint accounts deserve special caution. Families often add an adult child to an account because the bank says it is simple. It is simple. It also changes ownership rights in ways many parents do not intend. I have seen that shortcut create as many disputes as it solves.

Trusts can work well for families with real property, multiple accounts, or a child already serving in a trustee-type role. But a trust only controls assets that were transferred into it. An unfunded trust binder on a shelf does not solve a banking problem.

Medical powers, HIPAA releases, wills, and beneficiary reviews also matter. They address different decisions, and they often prevent the second wave of conflict that hits after the immediate financial crisis passes.

What works best in real life

The families who avoid guardianship usually do two things early. They sign the right documents while the parent still understands what they are signing, and they test those documents before a crisis by confirming what the bank, brokerage firm, or title company will require.

That second step gets overlooked all the time. A DPOA that sits in a drawer is only half a plan. A DPOA that has been reviewed, copied, and accepted by the institutions involved is much more likely to hold up when the call comes from the hospital or rehab facility.

When Texas Guardianship Is the Only Option

Sometimes the parent never signed a DPOA. Sometimes they signed one, but the document is defective, too narrow, or under attack by another family member. Sometimes a bank refuses to honor it because the institution wants additional proof, and the parent is no longer able to clarify or sign anything new. In those cases, families have to look at guardianship.

Texas guardianship is a court-created relationship under Title 3, Subtitle G of the Texas Estates Code. The court appoints a guardian for an incapacitated person, called the ward. For financial control, the key tool is usually a guardianship of the estate. A guardianship of the person deals with personal decisions such as residence, care, and some medical issues.

Why courts treat guardianship as a last resort

Guardianship removes some decision-making rights from an adult. Because of that, Texas courts are supposed to consider whether a less restrictive alternative will work. If a valid DPOA, trust arrangement, supported decision-making structure, or other tool can adequately protect the parent, that option may be preferred.

But when no workable alternative exists, refusing to seek guardianship can leave a vulnerable adult exposed. A frozen account can be as dangerous as a stolen one if care bills, taxes, and housing costs go unpaid.

When guardianship becomes the responsible choice

Common situations include:

- The parent already lacks capacity and cannot sign new documents

- There is no valid DPOA

- The existing agent is suspected of abuse or self-dealing

- Family members are fighting over who should control funds

- Immediate court authority is needed to stop exploitation

Guardianship is not a shortcut. It is the formal answer when informal help and private planning can’t safely do the job.

Families often underestimate how heavy that process can be. As noted in guidance on taking over a parent’s finances during crisis situations, a contested guardianship can take many months and involve significant legal fees, while a power of attorney can often be put in place far more quickly if capacity still exists. That gap matters when a parent declines suddenly.

Temporary and emergency situations

If money is disappearing now, waiting for a standard case may not be realistic. Texas law allows forms of urgent relief, including temporary guardianship in appropriate cases. Whether that is the right move depends on the facts. A parent in a Harris County hospital after a stroke may need one type of filing. A parent whose caregiver is emptying accounts may need another.

The key point is practical. If the danger is immediate, get legal guidance immediately. The right filing depends on proof, timing, and the county court involved.

Navigating the Texas Guardianship Process Step by Step

A guardianship case starts in the proper court, usually the probate court or a court handling probate matters in the county where the proposed ward resides. In a place like Harris County Probate Court, procedure matters. Missing a document or serving the wrong party can slow everything down.

Texas also has a strong reason for imposing all this structure. Texas seniors filed more than 62,347 fraud complaints in a single year, reporting losses exceeding $1.35 billion, according to KHOU’s report on FBI senior scam data in Texas. Court-required inventories and annual accountings are not paperwork for paperwork’s sake. They create a record that helps protect the ward’s money.

Step one file the application

The process usually begins with an Application for Appointment of Guardian. The filing identifies the proposed ward, explains why guardianship is necessary, and states whether the request is for the person, the estate, or both.

This is also where less restrictive alternatives matter. The court will want to know why those options won’t adequately protect the parent.

Step two prove incapacity

The court needs evidence, not family opinion. In many adult guardianship cases, that means a physician’s Certificate of Medical Examination or other required proof showing the nature and extent of incapacity.

The legal standard matters because the court should tailor authority to the actual need. If the parent can still handle some tasks, the court may consider a limited guardianship instead of a broader one.

Step three the court appoints an attorney ad litem

Texas courts protect the proposed ward by appointing an attorney ad litem in many cases. That lawyer represents the ward’s interests, not the family’s wishes. The attorney ad litem meets with the proposed ward, reviews the circumstances, and reports to the court.

This surprises many families. They assume everyone in court will be working toward the same result. That isn’t how guardianship should work.

Step four expect investigation and a hearing

There may be a court investigation, notice requirements, and a hearing where the judge decides whether guardianship is necessary and who should serve. If more than one relative wants the role, the hearing can become contested.

For a practical overview of filing and court expectations, families often start with information about legal guardianship of a parent in Texas.

A short video can also help you visualize what the process looks like in practice.

Step five qualify and start complying

Being appointed is not the end. It is the beginning of a supervised role.

After appointment, a guardian of the estate may need to:

- Take an oath and qualify with the court

- Obtain a fiduciary bond if required

- Gather and protect assets

- File an inventory of the estate

- Maintain records for annual accountings

Texas Estates Code requirements in Title 3, Subtitle G are strict because a guardian is a fiduciary. That means the guardian must act for the ward’s benefit, keep funds separate, avoid self-dealing, and document transactions carefully.

What families should do before and after the hearing

Before the hearing:

- Collect records early: bank statements, deeds, bills, insurance records, and prior planning documents

- Coordinate with physicians: delays often start when medical proof is incomplete

- Prepare for family conflict: judges notice when relatives are disorganized or motivated by personal grievances

After the hearing:

- Use Letters of Guardianship correctly: many institutions will ask for current certified copies

- Calendar reporting deadlines: missed deadlines create court problems fast

- Keep clean books: every payment should be traceable

If the case touches probate-related property transfers or estate administration issues, families may also need guidance through the court system generally, including Texas Probate matters.

Your Duties Using Your Authority and Preventing Abuse

Once you have authority, whether as an agent under a DPOA or as a guardian of the estate, your job changes from “getting access” to using that access properly. However, good intentions are not enough. Banks, title companies, Social Security offices, and investment firms want the right document, the right identification, and sometimes their own internal forms.

What to say when a bank pushes back

Keep it simple and specific.

“I’m acting under a valid Durable Power of Attorney signed by my parent. I need your branch’s procedure for adding this document to the account file and confirming what additional forms you require.”

If you’re a guardian, the script is different:

“I’m the court-appointed guardian of the estate. Here are my current Letters of Guardianship. Please tell me what your institution needs to recognize the account authority.”

Don’t argue with front-line staff about what the law “should” be. Ask for the institution’s legal-process checklist, the document review department, or a supervisor. Many rejections are not final refusals. They are documentation problems.

Daily rules that keep you out of trouble

- Keep money separate: never mix the parent’s funds with your own

- Pay from the parent’s account when possible: that creates a clear record

- Save receipts and statements: especially for large or unusual expenses

- Avoid “borrowing” even temporarily: fiduciary authority is not personal access

- Tell siblings the basics when appropriate: secrecy often breeds disputes

Red flags that abuse may still be happening

Legal authority does not end the risk. It changes the way you monitor it.

Watch for:

- New credit activity your parent didn’t authorize

- Mail forwarding or address changes you didn’t request

- Unexpected beneficiary changes

- Caregivers asking for cash or gift cards

- Another relative pressuring the parent to sign new papers

If you suspect exploitation, report it promptly and speak with counsel about preserving records. Texas law treats elder financial exploitation seriously, and delay can make recovery harder.

The fiduciary standard is real

An agent under a DPOA and a guardian of the estate both owe duties of loyalty, care, and honesty. The court expects a guardian to follow orders closely. Financial institutions expect an agent to stay within the written powers granted. If you exceed that authority or use funds for yourself, you can face removal, civil liability, and in some cases criminal consequences.

The emotional truth is that taking legal control of a parent’s finances is rarely comfortable. It forces families to confront decline, family history, and fear. But handled correctly, it is an act of protection. It keeps the lights on, preserves housing, pays for care, and lowers the chance that a vulnerable parent will be exploited when they can least defend themselves.

If you’re facing this decision now, a short conversation with the right lawyer can save time, conflict, and avoidable mistakes. The Law Office of Bryan Fagan, PLLC helps Texas families evaluate whether a Durable Power of Attorney, temporary relief, or a full guardianship is the proper path, and offers free consultations so you can get guidance specific to your parent’s situation.