Skip to content

Skip to content Watching a parent's health decline is one of the most challenging experiences a family can face. Amid the emotional turmoil, you are often confronted with urgent financial questions: how do we protect the assets our parents worked their entire lives to build? In Texas, the answer involves a thoughtful mix of proactive legal tools like powers of attorney, trusts, and strategic Medicaid planning. When those are not in place, a court-supervised guardianship may be necessary. A proactive approach is the best way to ensure their savings are there for their care and are not depleted by the staggering costs of a long-term medical event.

This guide is designed to provide Texas families with clarity and direction. Our mission at The Law Office of Bryan Fagan is to help you navigate these sensitive issues with compassion and confidence, ensuring your loved ones are protected.

A Texas Family's Guide to Protecting Your Parents' Financial Future

It’s an emotional journey when a parent’s health begins to fade, and it forces you to confront difficult financial realities. For most Texas families, the biggest worry is simple: how do we prevent a lifetime of savings from being completely drained by the astronomical costs of long-term care?

This guide is meant to be your roadmap. We understand the emotional and financial challenges you face, and we want to help you take the right steps now to secure your parents’ future. This isn't about hiding money—it’s about loving and responsible planning to ensure they receive the best possible care while preserving the legacy they’ve built.

Understanding the Financial Reality of Long-Term Care

The need for this kind of planning has never been more critical. People are living longer, which means more seniors will need some form of assistance, and the price tag is shocking.

Consider this: roughly 70% of adults who reach age 65 will need some form of long-term care in their lifetime. As of 2024, the average cost for a private room in a nursing home is hovering around $127,750 a year. For families in major Texas hubs like Houston and Dallas, those national averages are a painful reality. If you want to dig deeper, you can review more long-term care statistics to really understand the financial impact.

This journey is complex, but you don't have to walk it alone. Our mission at The Law Office of Bryan Fagan is to provide clarity and compassionate guidance, helping you navigate Texas guardianship and estate planning laws with confidence.

Key Asset Protection Strategies at a Glance

Navigating legal options can feel like learning a new language. To simplify things, here is a quick look at the primary tools used in Texas to protect a parent's assets. Each serves a specific purpose and is best used at different times.

| Strategy | Primary Purpose | Best Used When |

|---|---|---|

| Durable Power of Attorney | Lets a trusted person manage finances if a parent becomes unable to do so themselves. | Your parent is still mentally sharp and can legally appoint someone to act on their behalf. |

| Irrevocable Trusts | Moves assets out of your parent’s name to shield them from creditors and help qualify for Medicaid. | You're planning well in advance, respecting Medicaid's 5-year look-back period. |

| Medicaid Planning | Legally structures assets to meet the strict eligibility rules for government-funded long-term care. | A nursing home stay is on the horizon or has already started (often called "crisis planning"). |

| Guardianship of the Estate | A court appoints someone to manage finances when a parent is incapacitated and has no prior planning in place. | This is truly a last resort when no other legal documents exist. |

This table is just the starting point. This guide will walk you through these strategies in more detail, giving you practical steps to make informed decisions for your family.

Of course, every family’s situation is unique. If you're feeling overwhelmed and need guidance tailored to your specific circumstances, we encourage you to schedule a free consultation with our experienced attorneys. We're here to help.

Understanding Your Parent's Current Situation

Before you can develop a legal strategy to protect your parents' assets, you must get a clear, honest picture of where things stand right now. This is the groundwork for everything that follows, and it requires patience, empathy, and a great deal of respect.

This isn’t about taking over. It’s about partnering with them to ensure their future is secure and their wishes are honored.

The first step is often the most difficult: starting the conversation. These talks can be incredibly delicate. Many parents cherish their independence and might be reluctant to discuss their finances. The key is to approach it from a place of love, framing it as a way to help them stay in control and ensure their wishes are followed, not as a power grab.

Recognizing the Early Warning Signs

Sometimes, the need for help doesn’t come with a formal announcement. It appears in small, subtle changes to daily life. Paying close attention to these shifts can be the first clue that your parents need more support managing their affairs.

For example, a family in Harris County might notice their mom, who was always meticulous with her finances, has started getting overdue bill notices. Or perhaps you stop by for a visit and see a pile of unopened mail on the kitchen counter. These are not just moments of forgetfulness; they are critical signals that it’s time to step in and offer support.

Other red flags to watch for include:

- Unusual Spending: Are there sudden, large withdrawals from their bank account? New credit cards you didn't know about? Uncharacteristic purchases can point to confusion, vulnerability to scams, or cognitive decline.

- Confusion About Accounts: If your parent seems hazy on their bank balances, investments, or insurance policies, it’s a strong sign that managing it all has become overwhelming.

- Neglected Property: A home falling into disrepair or a car with an expired registration can suggest they're struggling to keep up with essential responsibilities.

The Practical Step of Gathering Documents

Once you've opened the lines of communication, the next step is a practical one: helping them organize their essential documents. This process isn't just about tidying up; it provides the factual foundation for any future legal planning and is a core part of protecting their assets.

Going through these papers together can be a collaborative and reassuring activity. It gives you both a concrete understanding of their financial position and ensures that vital information is easy to find when it’s needed most, especially in an emergency.

Taking inventory of your parent's assets and legal documents is the first and most crucial step in creating a protection plan. Without a clear picture, you are navigating in the dark, unable to choose the right legal tools for their specific needs.

Here's a checklist of the key documents you'll want to locate and organize:

- Financial Records: Recent bank and brokerage statements, retirement account details (like 401(k)s and IRAs), and a list of all income sources, such as Social Security or pensions.

- Property Documents: Deeds to any real estate, vehicle titles, and statements for any mortgages or loans.

- Insurance Policies: Life insurance, long-term care insurance, and health insurance paperwork.

- Estate Planning Documents: Any existing Wills, Trusts, or Powers of Attorney. You absolutely need to know what’s already in place.

- Personal Information: Birth certificates, Social Security cards, and marriage certificates.

Taking this comprehensive inventory is what allows you to assess their situation accurately. It will clearly show what assets need protection, what legal plans they already have, and where the biggest vulnerabilities lie. From this starting point, you can move forward to build a solid strategy. If you feel overwhelmed trying to make sense of these documents, our team at The Law Office of Bryan Fagan is here to provide the personalized guidance you need.

Essential Tools for Proactive Planning

When your parent still has the mental clarity to make their own decisions, you're in a golden window of opportunity. This is the time to act. Being proactive now is the single best way to ensure their wishes are honored down the road, shielding their assets and saving your family the stress, expense, and emotional toll of a court-supervised guardianship.

These legal documents are the essential tools for getting ahead of a crisis. They are relatively straightforward, cost-effective, and ensure that if a medical emergency happens, a trusted person can step in immediately without any delay. This is how you keep control within the family and out of the courts.

The Cornerstone: Durable Power of Attorney

Think of a Durable Power of Attorney (DPOA) as the foundation of your parent’s entire asset protection plan. It's a legal document where your parent (the "principal") names someone they trust (the "agent") to handle their finances if they become unable to do so themselves.

The agent's power can be as broad as needed, from paying the mortgage and managing bank accounts to selling property and overseeing investments. The "durable" part is what makes it so powerful—it means the document stays in effect even after your parent loses the capacity to make their own decisions.

Imagine a mother in Dallas who appoints her son as her agent. If she later has a stroke and can't communicate, that DPOA lets him instantly access her bank accounts to pay for medical care and keep her household running. Without it, the family would almost certainly be headed to a Dallas County probate court for a lengthy and expensive guardianship proceeding just to get the same authority.

Directing Healthcare with a Medical Power of Attorney

While the DPOA covers finances, a Medical Power of Attorney (MPOA) is all about healthcare. This document lets your parent appoint an agent to make medical decisions for them if they can't. It’s about making sure their health preferences are respected by someone who knows them best.

The agent’s role kicks in once a doctor certifies that the parent is incapacitated. From that point on, they can talk to doctors, approve treatments, and review medical records. It’s a vital tool for ensuring good care continues and preventing family arguments during an already stressful time.

A common misconception is that family members automatically have the right to make medical decisions. That's not true in Texas. Without a Medical Power of Attorney, doctors and hospitals might require a court-appointed guardian, which can cause dangerous delays in care.

Other Essential Proactive Documents

Beyond those two core documents, a few others will round out a truly solid plan. Each one serves a specific and crucial purpose.

- Advance Directive to Physicians (Living Will): This document, outlined in the Texas Health and Safety Code, spells out your parent’s wishes for end-of-life care, such as whether they want life-sustaining treatment. It speaks for them when they can't, taking an incredible weight off the family's shoulders.

- HIPAA Release: The federal HIPAA law creates strict medical privacy rules. A signed HIPAA release gives specific people permission to access your parent's medical information, which is essential for talking with doctors and understanding their condition.

- Revocable Living Trust: For families with more complex assets, a trust can be a fantastic tool for managing property and avoiding probate court. You can learn more about how a living trust in Texas can add another layer of control and protection.

A huge piece of this puzzle involves planning for potential healthcare costs in retirement, as those expenses can quickly drain a lifetime of savings. By getting these essential documents in place now, you’re building a legal shield that protects your parent's choices and their assets. It’s an act of love that delivers incredible peace of mind.

Safeguarding Assets With Trusts and Medicaid Planning

When a power of attorney isn't enough to handle the crushing costs of long-term care, families must look at more powerful strategies. The hard truth is that a long stay in a nursing home can vaporize a lifetime of savings, leaving nothing for a surviving spouse or for heirs. This is exactly where tools like trusts and strategic Medicaid planning come into play.

These strategies are not about hiding money or cheating the system. They are about legally and ethically restructuring assets so your parent can qualify for the care they need while preserving what they worked so hard to build. This takes careful, forward-thinking action, often years before a crisis hits.

The need for this kind of private planning is only getting more critical. With public retirement systems under growing pressure, the burden of securing a financial future is falling more and more on individuals and their families. For Texans, Social Security and pensions should be seen as a starting point, not the whole safety net. This reality makes legal tools like trusts absolutely essential for protecting assets from future unknowns.

Revocable vs. Irrevocable Trusts: What's the Difference?

To understand trusts, you first need to know the two main types: revocable and irrevocable.

A Revocable Living Trust is flexible. Your parent can change it, move assets in and out, or even dissolve it completely. While it's a fantastic tool for avoiding probate and managing assets if your parent becomes incapacitated, it offers zero protection from nursing home costs or other creditors. Why? Because the assets are still legally considered your parent's property.

An Irrevocable Trust, on the other hand, is built for protection. Once assets are moved into it, your parent officially gives up ownership and control. That’s a big step. But it is this separation that shields the assets. For Medicaid planning, assets held in a properly structured irrevocable trust are no longer countable, which is crucial for qualifying for benefits.

Using an Irrevocable Trust for Medicaid Planning

The primary reason families use an Irrevocable Trust is to help a parent become eligible for Texas Medicaid to pay for long-term nursing home care. The costs are astronomical, and for most people, Medicaid is the only way to pay for an extended stay. The catch is that Medicaid has very strict asset limits—an individual can generally have no more than $2,000 in countable assets.

By moving assets like a house, savings, or investments into a specially designed Irrevocable Trust, you legally take them out of your parent’s name. This helps them "spend down" their assets to meet that $2,000 threshold without actually giving everything away to the nursing home.

Key Takeaway: Timing is everything. Texas, like every other state, has a five-year "look-back" period. This means Medicaid officials will scrutinize every financial transfer made in the five years before the application is filed. Any assets gifted or moved into a trust during that window can trigger a penalty period, delaying your parent's eligibility for benefits.

This is why "planning ahead" isn't just a catchy phrase—it's a requirement. A family in Fort Worth who puts their parents' home into a trust ten years before care is needed will almost certainly see that asset fully protected. A family that waits until their mom is on the verge of moving into a facility faces a much tougher road. We offer detailed guidance on protecting assets from nursing home costs and can help you make sense of these complex rules.

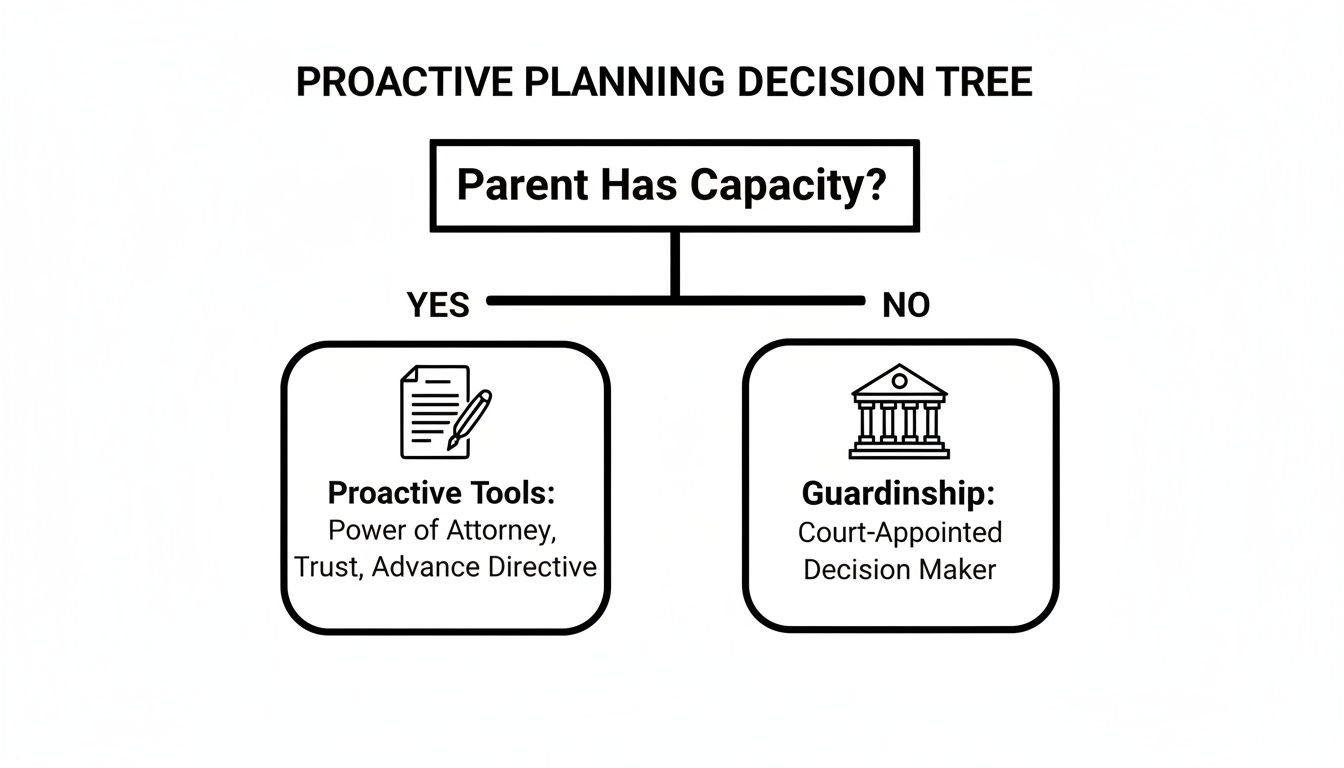

The decision tree below shows just how critical it is to act while your parent still has the mental capacity to make these major legal decisions.

As you can see, having capacity keeps proactive options like trusts on the table. Losing capacity often means the only path forward is a court-supervised guardianship.

Is It a Good Fit for Your Family?

An Irrevocable Trust is a serious commitment and it’s not the right tool for everyone. It means giving up a great deal of control over the assets placed inside it.

You really need to consider these factors:

- Health and Age: The younger and healthier your parents are, the better the odds are that you'll be safely outside that five-year look-back period when care is eventually needed.

- Asset Level: This strategy makes the most sense for families with moderate assets they want to protect, like the family home and a nest egg of savings.

- Family Dynamics: The person named as trustee (usually an adult child) has a massive responsibility. You must have a rock-solid foundation of trust and communication in your family for this to work.

Creating these kinds of advanced legal structures demands precision and a deep knowledge of Texas law. One wrong move can be incredibly costly, potentially disqualifying your parent from benefits right when they need them most. Working with an experienced Texas guardianship and estate planning attorney isn't just a good idea; it's the only way to ensure it’s done right.

Navigating Guardianship When It Becomes Necessary

Sometimes, despite our best efforts, a parent loses the ability to make sound decisions before legal plans are put in place. In these tough, emotionally charged situations, a court-supervised guardianship often becomes the only path forward to protect them and their assets.

While proactive planning is always ideal, think of guardianship as a powerful legal safety net when other options are off the table. It is a formal court process where a judge appoints a responsible person—the guardian—to manage an incapacitated person’s affairs when they can no longer do so themselves.

Understanding Guardianship in Texas

In Texas, guardianship cases are handled in probate courts, like those in Harris or Tarrant County. The entire process is governed by the Texas Estates Code, specifically Title 3, Subtitle G, which lays out all the rules, rights, and responsibilities.

The court can appoint a guardian for two distinct jobs, and sometimes one person handles both:

- Guardian of the Person: This person is responsible for your parent's physical well-being. They make decisions about medical care, where your parent lives, and their day-to-day care.

- Guardian of the Estate: This is the role focused on asset protection. This individual takes over your parent's financial life—paying bills, managing investments, protecting property, and ensuring their savings are safe from scams or poor decisions.

For families concerned about protecting an elderly parent's assets, the Guardian of the Estate provides the ultimate legal authority and, just as importantly, court oversight.

The Guardianship Process: Practical Steps for Families

Let's be clear: seeking guardianship is a major legal step. It involves asking a court to declare a person legally incapacitated, a decision no family takes lightly. The journey begins by filing a formal application with the appropriate probate court.

A typical case unfolds in these practical stages:

- Application: A family member files an application explaining why a guardian is necessary.

- Physician's Certificate: The court requires a recent letter from a physician confirming the parent's medical condition and their inability to manage their own affairs.

- Attorney Ad Litem: The court appoints an independent attorney, called an "attorney ad litem," to represent your parent's interests. This is a crucial step to protect their rights.

- Hearing: A judge holds a hearing to review all evidence, including the doctor's report and testimony from family, before making a final decision.

Our firm helps families understand how to obtain guardianship of a parent, walking them through each part of this complex process with compassion and legal precision.

It’s a common misconception that guardianship is a simple matter of filling out forms. The reality is that it’s a formal lawsuit designed to strip away a person's rights for their own protection. It is a last resort, but an absolutely necessary one when no other safeguards are in place.

Guardianship vs. Power of Attorney: A Comparison

It’s easy to confuse these two powerful tools. A Durable Power of Attorney is a document your parent signs while they still have capacity, giving someone authority to act on their behalf. A guardianship is a court-imposed solution when your parent has already lost capacity and can no longer sign legal documents. This table breaks down the key differences.

| Feature | Durable Power of Attorney | Guardianship of the Estate |

|---|---|---|

| When It's Created | Signed by the individual while they have legal capacity. | Imposed by a court after an individual is found to be incapacitated. |

| Authority Source | The document itself grants authority. | A court order grants authority. |

| Oversight | No automatic court supervision; the agent acts independently. | Strict, ongoing court supervision is mandatory. |

| Public Record | Private document. | Public court proceeding and records. |

| Cost & Complexity | Relatively simple and inexpensive to create. | A formal, more complex, and costly legal process. |

| Reporting | No formal reporting required, unless demanded. | Guardian must file a detailed inventory and annual accountings. |

Understanding this distinction is critical. The Power of Attorney is proactive planning; guardianship is a reactive, court-driven protection.

Why Guardianship Is a Powerful Asset Protection Tool

With elder financial exploitation becoming a multi-billion-dollar problem, the oversight that a court provides has never been more vital. A formal guardianship creates a formidable defense against predators.

The Texas Estates Code imposes strict fiduciary duties on a Guardian of the Estate, requiring them to file a detailed inventory of every single asset and submit annual accountings for a judge's review.

This built-in court supervision means every financial decision is transparent and accountable. It dramatically reduces the risk that a parent's life savings will be drained by fraud, undue influence from a "new best friend," or just plain neglect. When it becomes clear that a parent can no longer safely manage their affairs and no power of attorney exists, seeking guardianship isn't just an option—it's a duty of care.

How a Texas Elder Law Attorney Can Help

Protecting a parent's assets is never a one-size-fits-all problem. It’s a deeply personal journey. The legal landscape in Texas is a maze of complex rules, and a small misstep can lead to permanent and costly consequences for your family. This is not a path you should walk alone.

When you partner with an experienced elder law attorney, you gain an advocate who ensures every decision is legally sound, strategic, and tailored to your family's unique situation. The most effective plans are built with professional foresight, not reactive panic.

Navigating Complex Legal Frameworks

Think of an attorney as your guide. Their first job is to analyze your parent’s specific financial situation and then help you choose the right tools for the job.

This isn't just about filling out forms; it's about strategy. This often involves:

- Drafting Powers of Attorney: Building these documents to be robust and fully compliant with Texas law is key to preventing them from being challenged when you need them most.

- Structuring Trusts: An attorney can design an irrevocable trust that meets the incredibly strict requirements for Medicaid eligibility while still protecting family property.

- Guiding You Through Guardianship: If guardianship is the only option, an attorney will manage the entire court process—whether in Harris County Probate Court or elsewhere—from filing the initial application to representing you at the hearing.

An attorney's true value is in translating dense legal language, like the rules found in the Texas Estates Code, into a clear, actionable plan. They help you sidestep common but devastating mistakes, like accidentally violating Medicaid's five-year look-back period, which could jeopardize your parent’s access to long-term care.

Don't wait for a crisis to force your hand. The choices you make now can secure your parent's quality of care, protect their legacy, and provide your entire family with invaluable peace of mind.

During what is almost always an emotional time, an attorney provides a necessary, objective perspective. They ensure every step taken is truly in your parent's best interest. Their expertise is what builds a legal shield that will stand up to scrutiny and protect what truly matters.

Protecting your loved ones is a profound responsibility. If you feel overwhelmed and aren't sure where to start, we're here to offer clarity and direction. Schedule a free consultation with the experienced attorneys at The Law Office of Bryan Fagan to discuss your family's needs.

Answering Your Pressing Questions

When you're trying to figure out how to protect your parents' assets, a lot of questions pop up. It's completely normal. Here are some straightforward answers to the questions we hear most often from Texas families just like yours.

Can I Use My Parent’s Money for Their Care with a Power of Attorney?

Yes, absolutely. When you are named as an agent under a Durable Power of Attorney, your primary duty is to act in your parent's best interest. This includes using their funds to pay for their needs—such as medical bills, in-home care, or home maintenance.

The key is to keep meticulous records of every single dollar spent. Never mix their money with your own. This is called commingling funds, and it can lead to serious legal trouble in Texas, including potential civil lawsuits and even criminal charges.

What Is the Difference Between Guardian of the Person and Guardian of the Estate?

This is a common point of confusion. In Texas, a guardianship can be split into two separate roles. A judge, for instance at the Tarrant County Probate Court, might appoint one person to handle both jobs, or split them between two different people.

Here’s the breakdown:

- Guardian of the Person: This person is in charge of your parent's physical well-being. They are the decision-maker for healthcare, living arrangements, and day-to-day personal needs.

- Guardian of the Estate: This individual manages the financial side of things. They are responsible for all of your parent's property, paying bills from the estate's funds, overseeing investments, and legally protecting all assets.

Is It Too Late to Protect Assets if My Parent Is Already in a Nursing Home?

While it’s always best to plan ahead, it’s almost never too late to take action. Even if your parent has already moved into a nursing home, an experienced elder law attorney can still implement "crisis Medicaid planning" strategies.

These are immediate, legally-sound moves that must be made quickly. We might look at converting countable assets into exempt assets (like paying off a mortgage), setting up a specialized Miller Trust to handle income that's over the limit, or using spousal protection rules to secure assets for the healthier spouse at home. In these situations, getting fast, professional legal advice is absolutely critical.

How Much Does It Cost to Set Up a Trust or Establish Guardianship?

These are two very different paths with very different price tags.

A trust is a proactive planning tool you pay for once, with the cost depending on its complexity. Guardianship, on the other hand, is a formal court process with ongoing expenses, like court filing fees, fees for your attorney and an attorney for your parent, and other court-ordered costs.

Guardianship might seem more expensive, and often is, but sometimes it's the only option left on the table to legally protect a parent who has already lost the capacity to make decisions and has no other plans in place.

Trying to figure all this out can be overwhelming, but you're not in this alone. The experienced attorneys at The Law Office of Bryan Fagan, PLLC are here to offer the clear, compassionate guidance your family deserves. Schedule a free consultation today to build a plan that protects your parents and brings you some much-needed peace of mind.