Skip to content

Skip to contentFacing the reality of long-term care can feel overwhelming, especially when you consider the potential impact on a lifetime of savings. For many Texas families, the high cost of nursing home care can deplete a nest egg in just a few years. Protecting your assets from these costs is not just a financial strategy; it's a crucial step to secure your family's future. This requires a proactive legal plan, often involving tools like Medicaid planning and specialized trusts, to ensure your legacy is preserved while your loved ones receive the care they deserve.

We understand the emotional and financial weight of these decisions. This guide will walk you through essential steps and legal strategies with the clarity and care your family needs, empowering you to navigate this complex journey with confidence.

The Financial Shock of Long-Term Care in Texas

Watching a parent or spouse’s health decline is one of life's most difficult experiences. The emotional toll is heavy, and when you begin to see the staggering cost of long-term care, that emotional crisis can quickly become a financial one.

For the families we guide in Harris County, Dallas County, and across Texas, these numbers are often a harsh awakening. The financial future you carefully built can start to unravel with shocking speed. The need for a plan isn't a distant "what if"—it's an urgent reality that requires thoughtful action.

There’s a common—and dangerous—misconception that Medicare or private health insurance will cover an extended stay in a nursing facility. The hard truth is, they generally do not. This often leaves families paying out-of-pocket until their resources are almost completely drained, at which point they might finally qualify for Texas Medicaid.

Understanding the Numbers

This financial strain isn't just a possibility; it's a statistical reality. National data paints a stark picture: the average annual cost for a semi-private room in a U.S. nursing home hovers around $117,000, with a private room averaging $133,000.

Worse yet, those figures are projected to climb significantly in the coming years. If you want to see the full projections, you can explore the nursing home care data for yourself.

This is precisely why protecting assets from nursing home costs is so critical. Without a legally sound strategy, a family’s home, savings, and investments are all on the line.

Your Path Forward: Key Legal Strategies

Fortunately, Texas law provides several powerful tools to help families prepare. A comprehensive plan is about more than just saving money; it's about legally restructuring your assets so they are shielded from being counted for Medicaid eligibility. This is where an experienced Estate Planning attorney becomes your most valuable ally.

To help you get started, here's a quick look at the primary legal tools we use to protect assets for Texas families.

| Strategy | Primary Goal | Best For |

|---|---|---|

| Texas Medicaid Planning | Structuring finances to meet Medicaid's strict income and asset limits without having to spend everything down. | Families who anticipate needing long-term care within the next 5-7 years and want to qualify for assistance. |

| Irrevocable Trusts (MAPT) | Moving assets out of your name and into a trust, making them inaccessible for Medicaid qualification purposes. | Protecting major assets like a primary residence, vacation home, or significant investment accounts well in advance. |

| Spousal Protections | Using legal rules to ensure the healthy spouse living at home (the "community spouse") is not left impoverished. | Married couples where one spouse requires nursing home care while the other remains at home. |

| Permitted Asset Transfers | Legally transferring certain assets to specific individuals (like a disabled child) without violating the look-back rule. | Situations involving unique family circumstances, such as caring for a dependent with special needs. |

These strategies, when implemented correctly, can make all the difference. In this guide, we'll dive deeper into each one.

Navigating this process alone is incredibly risky. I’ve seen simple mistakes—like gifting money to a child or selling a home for a dollar—trigger a devastating penalty period. This can leave a loved one without coverage right when they need it most.

Thinking about these issues is never easy, but taking action now brings incredible peace of mind. By understanding your options, you can move from a place of anxiety to one of empowerment. For personalized guidance on your family's unique situation, we invite you to schedule a free consultation with our team.

Making Sense of Texas Medicaid and Its Five-Year Look-Back Period

For many Texas families, Medicaid is the only viable path to affording long-term nursing home care. However, qualifying for these benefits isn’t as simple as filling out a form. The Texas Health and Human Services Commission enforces strict income and asset limits, which can make families feel like they must spend every last dime to become eligible.

The single most important rule to understand is the five-year look-back period.

When you apply for Medicaid to help with nursing home bills, the state will closely examine your finances. Officials will scrutinize every transaction you have made for the 60 months immediately preceding your application date. This is a deep dive into bank statements, property sales, and investment accounts.

The purpose of the look-back is to prevent individuals from giving away their assets to family members simply to appear "poor" enough to qualify for Medicaid.

The Heavy Price of the Transfer Penalty

If the state finds any transfers made for less than fair market value during that five-year window, it will impose a transfer penalty. This isn't a monetary fine; it's a period of ineligibility during which Medicaid will not pay for your care.

For example, imagine a family in San Antonio whose father needs to move into a nursing home. Two years before applying for Medicaid, he gifted his children $120,000. When the application was submitted, the state took the $120,000 gift and divided it by the average daily cost of nursing home care in Texas—a figure set by the state, currently around $200 per day.

The result was a 600-day penalty period. For nearly 20 months, the father was ineligible for Medicaid benefits, forcing his family to cover the massive nursing home bills entirely out of pocket.

This is a scenario we see all too often in Harris County Probate Courts and across Texas. A well-intentioned gift, made with love, ends up creating a devastating financial crisis precisely when a family is most vulnerable.

Understanding these rules is about ensuring your loved one can get the care they need. Any uncompensated transfer—whether it’s cash, a car, or the family home—can trigger this penalty.

Common Mistakes That Trigger Penalties

Many seemingly innocent financial moves can cause problems with Medicaid eligibility. It is critical to know what the state considers an improper transfer:

- Giving large cash gifts to children or grandchildren for a wedding, a down payment on a house, or other milestones.

- Selling a home or a car to a relative for a token amount, like $1, instead of its actual fair market value.

- Adding a child’s name to your bank account or the deed to your house. This is often viewed as gifting a portion of that asset.

- Paying for a grandchild's college tuition directly from your savings.

Each of these actions, even when done with the best intentions, can lead to a long and costly period of Medicaid ineligibility. This is why careful planning and meticulous record-keeping are non-negotiable.

The Only Real Solution Is to Plan Ahead

The five-year look-back rule makes one thing crystal clear: you cannot wait until a crisis to start protecting your assets. The most effective strategies must be implemented long before nursing home care becomes an immediate need.

Planning ahead gives you the full advantage of the five-year window, allowing you to legally and ethically reposition assets so they are protected without triggering a future penalty.

As you explore your options, it's also wise to learn about other types of available support. We have created a detailed guide on the Medicaid waiver program in Texas, which explains programs that can provide care outside of a nursing home.

Navigating these complex rules alone is a recipe for disaster. If you are concerned about how past financial decisions could impact future eligibility, you need professional advice. Our team can help you understand the look-back period and build a strategy that works within Texas law.

Using Trusts to Safeguard Your Family's Legacy

While navigating Medicaid's rules can feel reactive, proactively protecting your assets is where you can truly find peace of mind. One of the most powerful tools in an estate planner's toolkit is the strategic use of legal trusts. They allow you to legally separate assets from your name, shielding them from being counted by Medicaid and preserving them for your family.

It's absolutely crucial to understand that not all trusts are created equal for this purpose. Many people already have a revocable living trust as part of their basic estate plan. While these are excellent for avoiding probate, they offer zero protection against nursing home costs. Why? Because you retain full control over the assets, and for Medicaid's purposes, anything you control is still considered yours.

The Power of Irrevocable Trusts

To get real asset protection, you need a very specific tool: an irrevocable trust. As the name suggests, once you place assets into this kind of trust, you legally give up direct control and ownership. This is the essential step that removes them from your "countable assets" when Medicaid runs its calculations.

The most common and effective version we use for this is the Medicaid Asset Protection Trust (MAPT). Think of it as creating a secure vault for your most significant assets, like your home or investment accounts, well before you ever need care.

Let's walk through a common scenario. Imagine a couple in Austin who owns their home outright. They work with an attorney to create a MAPT and transfer the deed of their home into it.

- The parents can continue to live in the home for the rest of their lives.

- They can still keep their valuable Texas homestead property tax exemptions.

- Critically, because the home is now legally owned by the trust, it's no longer a countable asset for the parents.

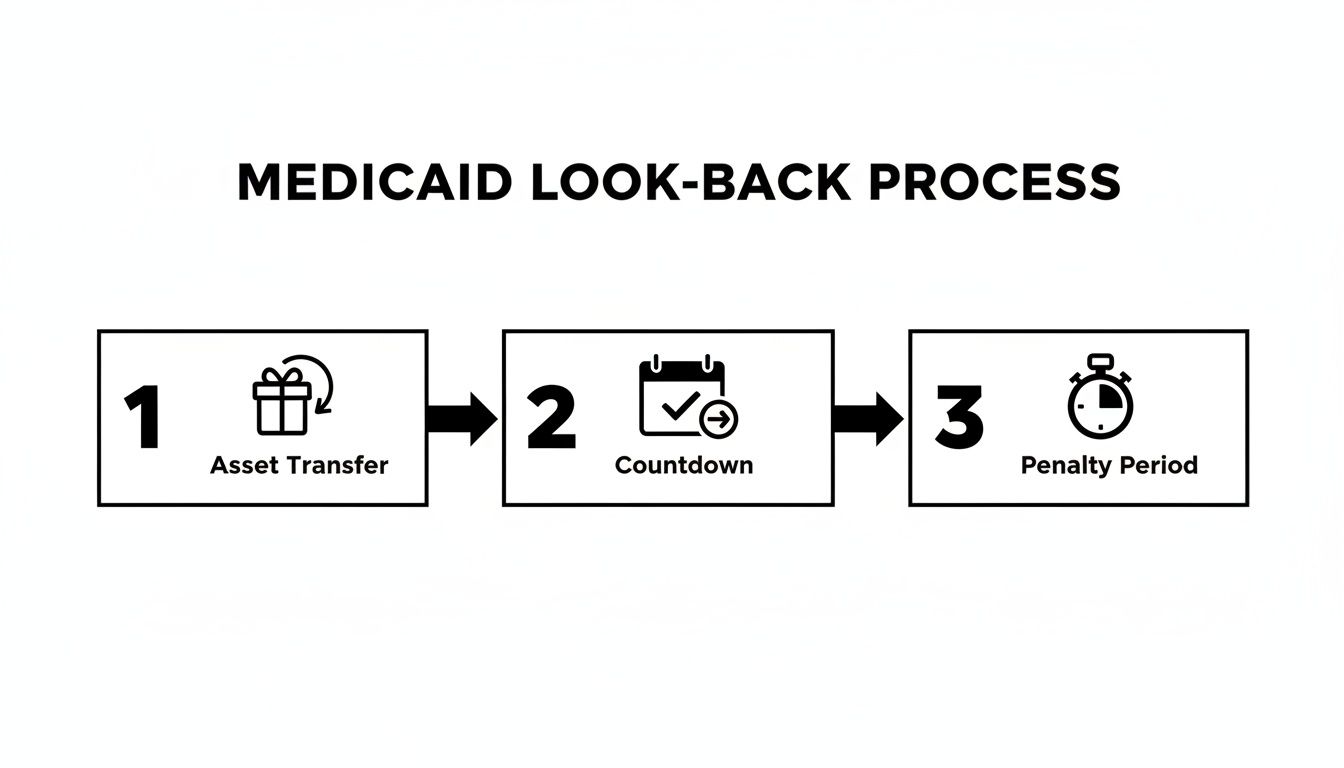

This single, proactive move ensures the family home—often the largest asset a family owns—is preserved for the next generation instead of being sold off to pay for long-term care. But there's a catch: timing is everything. This transfer has to be done well in advance to outlast the five-year look-back period.

This infographic shows exactly how that asset transfer starts the clock on the Medicaid look-back period.

The visualization makes it crystal clear. The moment an asset is transferred, the five-year countdown begins. Failing to plan far enough ahead can trigger a lengthy penalty period where no benefits are available, even if you desperately need them.

Protecting Loved Ones with Special Needs

Another vital tool in our arsenal is the Supplemental Needs Trust (SNT), often called a Special Needs Trust. This trust is designed for a very specific and compassionate purpose: to provide for a loved one with a disability without jeopardizing their eligibility for essential government benefits like Medicaid or Supplemental Security Income (SSI).

For instance, a grandparent in Fort Bend County wants to leave an inheritance to her adult grandchild who has a disability and relies on government benefits. If she leaves that inheritance directly to him, it would push him over the strict asset limits, causing him to lose his healthcare and income support—a devastating outcome.

By placing the inheritance into a properly drafted Supplemental Needs Trust instead, the funds can be used to pay for things that enhance the grandchild’s quality of life—like specialized therapy, education, or even travel—without ever being counted as his personal asset.

This is a profound act of care that protects both the inheritance and the beneficiary's well-being. Creating a special needs trust in Texas requires strict adherence to legal standards laid out in the Texas Estates Code, which makes professional guidance absolutely essential.

Setting up these sophisticated trusts is not a DIY project. The rules are incredibly complex, and a single mistake can completely undo the protections you're trying to create. An experienced attorney can ensure your trust is structured correctly under Texas law to truly safeguard your family’s legacy for generations to come.

Making Sure Spouses and Veterans Are Protected

When protecting assets from nursing home costs, some situations require a specialized approach. Two of the most common scenarios involve married couples where one spouse needs care, and veterans who have earned benefits through their service.

These situations come with unique rules and opportunities. Knowing how to navigate them correctly can provide immense financial relief and security for your family.

Preventing Spousal Impoverishment in Texas

For married couples, the fear that one spouse’s illness will bankrupt the other is all too real. Thankfully, Texas Medicaid law includes specific provisions—known as the Spousal Impoverishment Rules—to prevent that from happening. They are designed to ensure the healthy spouse who is still living at home (often called the "community spouse") isn't left financially devastated.

At the heart of these protections is the Community Spouse Resource Allowance (CSRA). This rule allows the healthy spouse to keep a significant portion of the couple's combined assets without disqualifying the spouse in the nursing home from receiving Medicaid. The exact amount changes each year, but it can be well over $150,000.

Let's walk through a quick example to see how this plays out.

Imagine a husband and wife in Harris County with $200,000 in countable assets. The husband suddenly needs to enter a nursing home. Without these protections, they would have to spend nearly all of their life savings down to the $2,000 Medicaid limit.

But with the CSRA, the wife (the community spouse) can keep her protected share of the assets. The rest would then be spent down on care costs until the couple hits the Medicaid eligibility threshold. This is how the wife avoids losing her financial security while her husband gets the care he needs.

These rules are a lifeline, but they aren't automatic. You have to structure your assets and application correctly to take full advantage of them. One misstep can lead to an unnecessary spend-down, completely defeating the purpose of the law.

Understanding these rules is a critical piece of any married couple’s asset protection strategy. It’s the key to ensuring that caring for one spouse doesn’t mean impoverishing the other.

Unlocking VA Benefits for Long-Term Care

For veterans and their surviving spouses, there's another powerful—and often overlooked—tool: the VA Aid and Attendance pension. This is a special monthly payment for eligible veterans who need help with daily activities like bathing, dressing, or eating.

It's designed specifically to help cover the costs of long-term care, whether that's at home, in an assisted living facility, or in a nursing home.

This benefit can provide thousands of dollars each month, completely tax-free, which significantly eases the financial load of long-term care. It acts as another crucial layer of support that can be used alongside other planning strategies.

To qualify for Aid and Attendance, a veteran or their surviving spouse must meet a few key criteria:

- Service Requirements: The veteran must have served at least 90 days of active duty, with at least one of those days during a period of war.

- Medical Need: A doctor must certify that the applicant needs daily help from another person for their personal care.

- Financial Need: The VA has its own income and asset limits, but they're generally much more lenient than Medicaid's.

For many Texas families, the Aid and Attendance benefit can be combined with Medicaid planning. The VA pension can help pay for care during Medicaid's five-year look-back period or supplement care costs once Medicaid kicks in. An integrated approach like this provides the most robust financial safety net possible.

Navigating the rules for both spousal impoverishment and VA benefits is a real challenge. The applications are detailed, and the laws are incredibly specific. For personalized help understanding your family’s options, a free consultation can give you the clarity and direction you need.

Exploring Your Full Range of Planning Tools

A solid plan to protect your life savings from nursing home costs isn't about a single solution. The most effective plans weave together multiple legal tools to create a comprehensive safety net that works for your family. By understanding the full range of options, you can build a resilient strategy that truly fits your life.

A key piece of this puzzle, while not a legal strategy itself, is long-term care insurance. This is a private insurance product designed specifically to cover the high costs of nursing homes, assisted living, or even in-home care.

Buying a policy when you're younger and healthier—in your 50s or early 60s—can be a cost-effective way to fund future care without ever needing to drain your assets to qualify for Medicaid. It provides more choice and control over the care you receive. To get a better handle on what's available, it's worth exploring various long-term care insurance options.

Permitted Asset Transfers Under Texas Law

While Medicaid’s five-year look-back period is designed to penalize most gifts, Texas law does carve out some important exceptions. These are specific situations where you can transfer assets without triggering a penalty period, but they require absolute legal precision.

A powerful example is transferring assets to a disabled child. Under both federal and Texas law, you can transfer any asset—including your family home—to a child who is certified as blind or permanently and totally disabled. This exception can protect a significant inheritance for your child while ensuring their needs are met, and it won't cause a period of Medicaid ineligibility for you.

This isn't a simple handshake deal. The transfer must be structured perfectly and documented with meticulous detail to satisfy the Texas Health and Human Services Commission. You absolutely need an attorney to get this right and avoid disastrous unintended consequences.

Another critical exception involves what's known as a "caretaker child." If your adult child lived in your home and provided care that kept you out of a nursing facility for at least two years right before you needed that level of care, you might be able to transfer the home to them penalty-free.

These are just a couple of examples. Tools like a Lady Bird Deed can also play a vital role in protecting your primary residence. We cover this in depth in our guide on how to get a Lady Bird Deed form in Texas.

When a Guardianship of the Estate is Necessary

Sometimes, planning is delayed until a person has already lost the mental capacity to make their own financial decisions due to dementia or another illness. In these crisis situations, they can no longer sign legal documents like a trust or a power of attorney. This is where a Guardianship of the Estate becomes unavoidable.

A guardianship is a formal legal process where a court, like one of our Harris County Probate Courts, appoints a responsible person (the "guardian") to manage the financial affairs of the incapacitated individual (the "ward"). Governed by Title 3, Subtitle G of the Texas Estates Code, the guardian is granted the legal authority to protect the ward's assets and apply for Medicaid on their behalf.

This court-supervised path is often the only option left to implement asset protection strategies when someone can no longer act for themselves. While it's more complex and public than planning ahead with a power of attorney, it is an essential tool for protecting a vulnerable loved one in a crisis.

However, a well-drafted Durable Power of Attorney can often prevent the need for guardianship altogether. By creating this document while you are still competent, you appoint a trusted agent to manage your finances if you become unable to do so. This empowers your agent to work with an attorney and execute the very asset protection plan you designed, sidestepping court intervention entirely.

Common Missteps Texas Families Make and How to Avoid Them

When protecting your life savings from long-term care costs, what you don't know can absolutely hurt you. We have seen countless well-meaning families make devastating mistakes, often stemming from a simple desire to do the right thing without understanding the legal consequences.

Learning from these common errors is one of the smartest ways to safeguard your own future. The biggest misstep we see, time and again, is waiting for a health crisis to strike before seeking legal advice. By then, your options have dwindled, forcing you into reactive, and often incredibly expensive, decisions. Proactive planning isn’t just a good idea; it’s the only reliable way to protect what you’ve worked so hard to build.

The Pitfall of DIY Gifting and Transfers

A classic—and damaging—mistake is trying to handle asset transfers without proper legal guidance. It’s a common belief that you can just give your assets away to your kids to qualify for Medicaid. This is a dangerous myth.

For example, a parent in Dallas might decide to sell their home to their child for a token amount, say $1, thinking this gets the house out of their name. Or maybe they add their son or daughter as a joint owner on their bank account, seeing it as a simple way to pass money along.

These moves might seem logical, but to Medicaid, they are improper transfers. They fly in the face of the five-year look-back rule and will trigger a substantial penalty period. This leaves your loved one without coverage and the family scrambling to pay for care out-of-pocket.

These "simple" transactions spiral into complex legal and financial headaches. Selling a home for less than its fair market value guarantees a penalty. And adding a child to a bank account? That can expose your life savings to their creditors, a lawsuit, or even a messy divorce settlement.

The True Cost of Informal Care

Many families try to shoulder the immense burden of care themselves. While this comes from a place of love, it can drain a family’s resources just as quickly as a nursing home. Globally, informal care provided by family can account for up to 50% of total long-term care spending when you factor in lost wages and missed opportunities.

And it's not just planning errors you need to worry about. External threats are very real. Taking the time for understanding and preventing elder financial abuse is critical, as scams and exploitation can wipe out a senior's savings and completely derail any asset protection strategy you have in place.

The Correct Approach: Sound Legal Strategy

Instead of these risky DIY moves, there are legally sound strategies that actually work.

- Instead of selling the house for $1, a properly structured Medicaid Asset Protection Trust or a Lady Bird Deed can protect the home without triggering penalties.

- Instead of adding a child to a bank account, a Durable Power of Attorney allows them to manage your finances on your behalf without co-owning the funds and exposing them to risk.

These strategies require precision and a deep knowledge of Texas law. The emotional and financial stakes are just too high to go it alone. Consulting an experienced Texas Guardianship and Probate attorney is the only way to be sure you're protecting what you’ve built. For personalized guidance on avoiding these common pitfalls, schedule a free consultation with our team.

Common Questions About Asset Protection in Texas

When it comes to protecting your family's legacy, it's natural to have questions. Here are the answers to some of the most common concerns we hear from Texas families navigating the complexities of long-term care costs.

Is It Too Late to Protect Assets If My Parent Is Already in a Nursing Home?

This is a very common concern, and the answer is almost always no, it's not too late. While planning years ahead provides the most options, powerful crisis-planning strategies are available even after a loved one has entered a facility.

These last-minute strategies can still protect a significant portion of a family's assets. However, they are complex and time-sensitive. It is essential to seek immediate advice from a qualified elder law attorney to preserve what you can.

Will Putting My House in a Trust Affect My Property Tax Exemptions?

This is a valid concern for any Texas homeowner. The good news is that with a properly drafted Medicaid Asset Protection Trust, you can often retain the right to live in the home and keep your valuable Texas homestead property tax exemptions.

The key phrase here is "properly drafted." The trust must be structured correctly under the Texas Estates Code to achieve this. This is why working with an experienced Estate Planning attorney is non-negotiable. A DIY trust from the internet could easily cost you these crucial benefits.

Can I Just Give My Assets to My Children to Qualify for Medicaid?

Please, do not do this. This is one of the most common and damaging mistakes families make. Giving away assets within five years of applying for Medicaid will almost certainly trigger a severe penalty period.

This penalty will make your loved one ineligible for benefits precisely when they need them most. While there are specific, legal ways to transfer certain assets without penalty, simply gifting them away is not one of them. It’s a move that can create devastating and long-lasting consequences for your family’s financial security.

Navigating these rules requires a trusted legal partner who knows the Texas system inside and out. The attorneys at The Law Office of Bryan Fagan, PLLC are dedicated to helping Texas families protect their legacies with compassionate, knowledgeable guidance. If you're facing the overwhelming challenge of long-term care costs, don't try to go it alone. Schedule your free consultation today so we can create a clear path forward for you and your family.